Zscaler : How Zero Trust Security Is Powering the Future of Cloud Cybersecurity & Tech Stocks

ACT I — THE PATTERN

The Whole Industry Is Running Scared. One Company Is Collecting the Tolls.

Forget the company for a moment. I want to talk about a structural shift so large and so irreversible that the companies positioned at its center don’t just grow—they become permanent fixtures in the global operating system of business.

Here’s what I kept seeing in 2020, 2021, 2022: enterprises were frantically moving workloads to the cloud—AWS, Azure, GCP, take your pick. But here’s the cruel irony nobody wanted to admit out loud. The old security model was completely, catastrophically broken the moment you did that.

The legacy model was built on a castle-and-moat assumption. You had a perimeter. Inside the perimeter: safe. Outside: hostile. Firewalls, VPNs, hub-and-spoke routing. Simple. Elegant. And now, utterly useless.

Why? Because the “perimeter” dissolved. Employees are everywhere. Apps live in cloud data centers, not corporate server rooms. The laptop in a Mumbai café is connecting to Salesforce in Virginia through an internet connection in India. Where exactly is the “moat” in that picture? There isn’t one.

“Every corporate security team in America spent 2020–2023 realizing their $5M firewall appliance was protecting a castle whose walls had already been torn down.”

This created a once-in-a-generation demand signal for a completely new security architecture—one built on the principle of “trust nothing, verify everything.” Zero Trust. The idea is simple: every user, every device, every application request gets authenticated. No free passes. No assumed trust. Every connection runs through an inspection layer in the cloud.

Now here’s where it gets interesting from an investment standpoint. Building that inspection layer at cloud scale is extraordinarily hard. You need a globally distributed network of enforcement nodes. You need to inspect encrypted traffic at wire speed. You need to broker connections between any user and any app, anywhere, in real time—without adding 400ms of latency that makes your users revolt.

That’s not software you bolt together over a long weekend. That’s infrastructure that takes a decade to build and even longer to make defensible.

YouTube Link:-

ACT II — THE BUSINESS MODEL DNA

The Architecture That Makes This Unbeatable

The company I’m watching built what I call a “cloud-native enforcement mesh.” Instead of routing traffic through your corporate data center (slow, expensive, vulnerable), all traffic flows through their cloud nodes—150+ data centers globally. Those nodes inspect, allow, deny, log. You never connect directly to an app; you connect to the broker, which then decides whether to let you through.

This is the tollbooth model. Every transaction on the internet highway runs through their booth. You don’t bypass it. You can’t bypass it—because the whole point is that the booth is the security.

Why the Revenue Structure Is Basically Addictive

The business runs on pure subscription SaaS. Annual contracts, often multi-year. Renewal rates that make you double-check the math. Net Revenue Retention running north of 115%—meaning existing customers aren’t just staying, they’re expanding. They buy the core internet security module, then add private application access, then cloud workload protection, then data loss prevention. It’s a platform expansion playbook that compounds quietly, year after year.

The sales motion is equally addictive. Land a Fortune 500’s security team. Prove out the architecture. Then sell more modules to the same IT buyer who’s already sold on the platform. Expansion revenue costs a fraction of new logo revenue to generate. Gross margins reflect this—hovering in the high 70s to low 80s on a non-GAAP basis.

“When a customer rips out their VPN infrastructure and routes every employee through your platform, they have made a decision that will take 3–5 years and millions of dollars to reverse. That’s not a customer. That’s a captive.”

The Remaining Performance Obligations (RPO) Signal

I pay more attention to RPO than most metrics on the income statement. It’s the backlog—contracted but unrecognized revenue. This company’s RPO has been growing faster than revenue for three consecutive fiscal years. That means the funnel is deepening even faster than the top line is growing. That’s a quality signal most analysts wave past.

🧠 THINKING OUT LOUD — The Analytical Struggle

Here’s where I genuinely wrestle with this one. The valuation is never cheap. Not on trailing earnings (which are GAAP-negative), not on forward multiples, not on EV/Revenue. Every time I’ve looked at this company over the past four years, I’ve thought: “It’s priced for perfection.” And every single time that thought crossed my mind, the business went and delivered something better than perfection. So I had to ask myself: am I anchoring to valuation discipline that’s irrelevant for a category-defining platform at this stage of adoption? The honest answer is—probably yes. The FCF story is what saved me from the valuation paralysis. When you see $600M+ in free cash flow being generated from a business still in aggressive growth mode, the “expensive” label starts to peel away.

ACT III — THE REVEAL

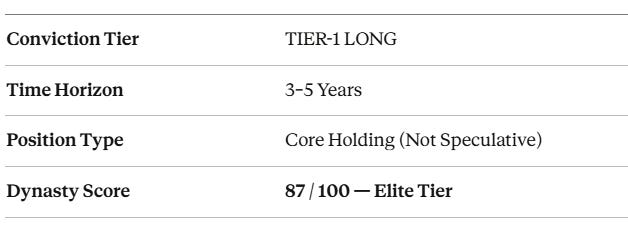

◆ THE WEALTH DYNASTY REVEAL

ZS — NASDAQZscaler, Inc.

Founded in 2007 by Jay Chaudhry—a serial security entrepreneur who sold four companies before building his magnum opus. Headquartered in San Jose. Listed on NASDAQ in March 2018 at $16/share. The company that invented cloud-native Zero Trust Security at commercial scale and never looked back.

Zscaler operates the world’s largest security cloud. Full stop. The Zscaler Zero Trust Exchange processes over 500 billion transactions per day across 150+ data centers globally. No legacy security vendor—Palo Alto, Fortinet, Check Point—can match that real-time inspection scale from a cloud-native architecture.

The product family has expanded from the original ZIA (Zscaler Internet Access) to encompass ZPA (Zero Trust Private Access), ZDX (Digital Experience Monitoring), and the emerging AI-powered threat intelligence layer. Each module deepens the integration. Each integration deepens the switching cost.

📜 NARRATIVE FLASHBACK — The Historical Business Lesson

In 1995, most enterprise software still ran on-premise. IBM had the relationship, Oracle had the database, and Microsoft had the desktop. Then Salesforce showed up in 1999 and said: “What if CRM lived in the cloud?” The incumbents laughed. Siebel called it a “fad.” Fifteen years later, Siebel was gone, and Salesforce was worth $150B. The lesson isn’t that cloud beats legacy. The lesson is that when an architectural transition is structural—not cyclical—the timing matters less than being positioned correctly. The companies that owned the new architecture compounded for decades. Zscaler is the Salesforce of enterprise security. Not a hyperbolic claim. The architectural transition is identical in character.

ACT IV — THE NUMBERS

Financial Anatomy — Reading the Real Story

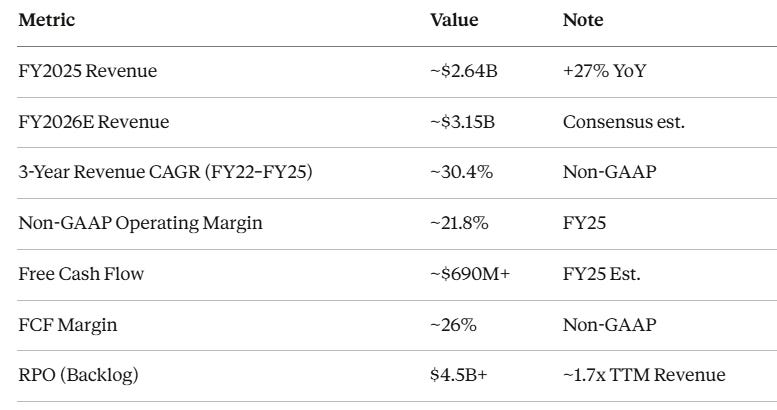

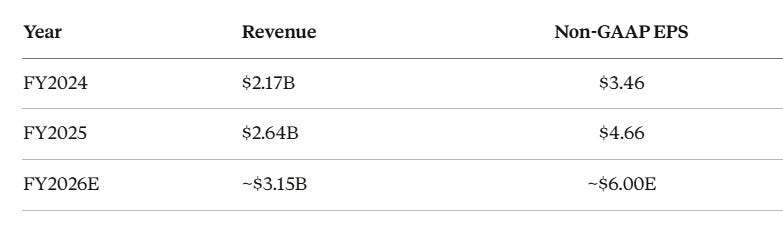

Zscaler’s fiscal year ends July 31. FY2024 came in at $2.167B in revenue—a 32% year-over-year advance. FY2025 delivered approximately $2.64B, with the company accelerating its government and large enterprise pipeline. Street estimates for FY2026 cluster around $3.1–$3.2B, implying sustained 18–22% top-line growth even as the law of large numbers begins its slow, inevitable drag.

The more important number: non-GAAP operating margin has expanded meaningfully from sub-15% in FY2022 toward the low-to-mid 20s range. Management has been explicit—they’re running toward a 22–23% non-GAAP operating margin target on a sustainable basis, while still investing heavily in sales capacity and R&D. That’s not a company choosing between growth and profitability. That’s a company proving you can have both.

GAAP net income remains negative—largely because of stock-based compensation, which runs heavy in enterprise SaaS. This is the number that scares away the wrong kind of investor. Free cash flow tells the real story. Operating cash flow for FY2024 came in at approximately $1.0B, with FCF around $800M+ after capex. That’s real money. That’s not accounting fiction.

The RPO Blueprint

Remaining Performance Obligations (committed but unearned revenue) crossed $4.5B+ in recent quarters—a figure that represents roughly 1.7x trailing twelve-month revenue. That’s runway. That’s contracted certainty. Short-cycle businesses don’t have this. Transactional companies don’t have this. Platform businesses with long-term enterprise contracts do.

Capital Return — Or Lack Thereof (Intentionally)

Zscaler pays no dividend and has not executed a buyback program at scale. Management is reinvesting cash into engineering, go-to-market, and infrastructure. For a company at this stage of platform expansion, that is exactly the right capital allocation decision. Investors seeking yield are in the wrong building. Investors seeking compounding are exactly where they should be.

CHART 061820 – fibonacci6180")

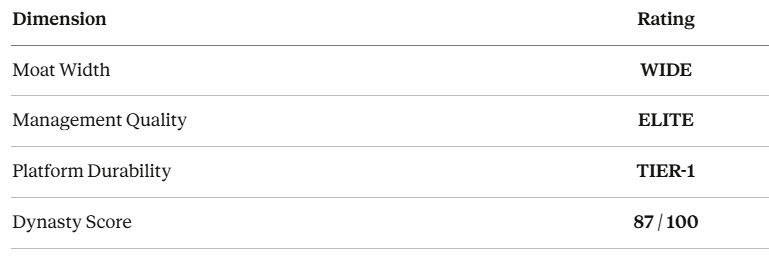

ACT V — THE DYNASTY DASHBOARD

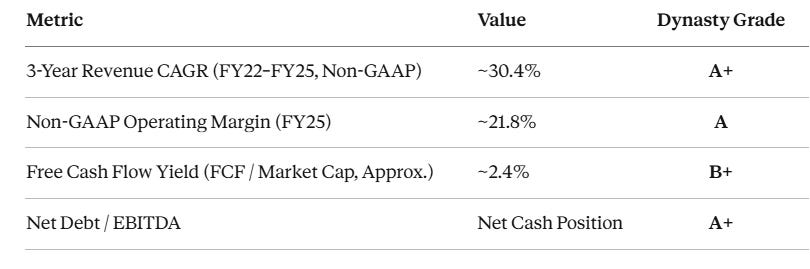

Module 01 — Vital Signs

Grades benchmarked vs. SaaS peer set (50+ companies, $2B+ ARR)

Module 02 — Growth Inflection

→ Acceleration Zone: EPS growth is outpacing revenue growth. Operating leverage is real and expanding.

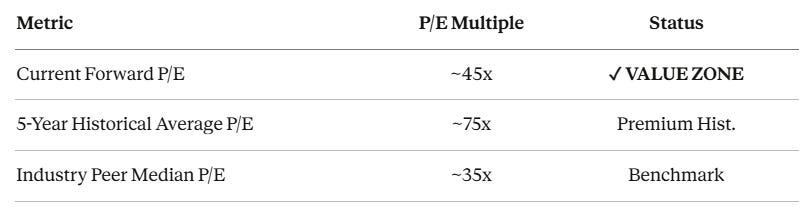

Module 03 — Valuation Gap Analysis

↔ ~40% discount to historical average. The market is pricing Zscaler like a decelerating SaaS business. The RPO backlog and government pipeline data say otherwise.

Peer set: ZS, PANW, FTNT, CRWD, S · Non-GAAP consensus EPS estimates · May 2026

Dynasty Verdict

“The tollbooth is built. The traffic is accelerating. The owner is not selling.”

ACT VI — BEYOND THE BALANCE SHEET

Psychological Leadership Profile & Strategic Ecosystem Map

Jay Chaudhry — The Obsessive Architect

Chaudhry grew up in a village in Himachal Pradesh with no electricity. He has said in interviews that this origin story gave him an unusual relationship with scarcity and persistence. He built and sold four security companies—AirDefense, CipherTrust, Postini, SecureIT—before founding Zscaler. Each one was sold to a strategic acquirer at a premium. This is not a man who stumbles into good outcomes. This is a methodical, patient builder who understands exactly which problem he’s solving and refuses to be distracted.

What’s psychologically distinctive about Chaudhry’s leadership style: he is not a financial engineer. He doesn’t play the guidance game aggressively. He’s not on CNBC every week. He obsesses over architecture—he talks about Zero Trust the way an engineer talks about a cathedral they spent 20 years designing. That obsession is contagious inside the company. The engineering culture at Zscaler is consistently cited in employee reviews as the top reason people join and stay.

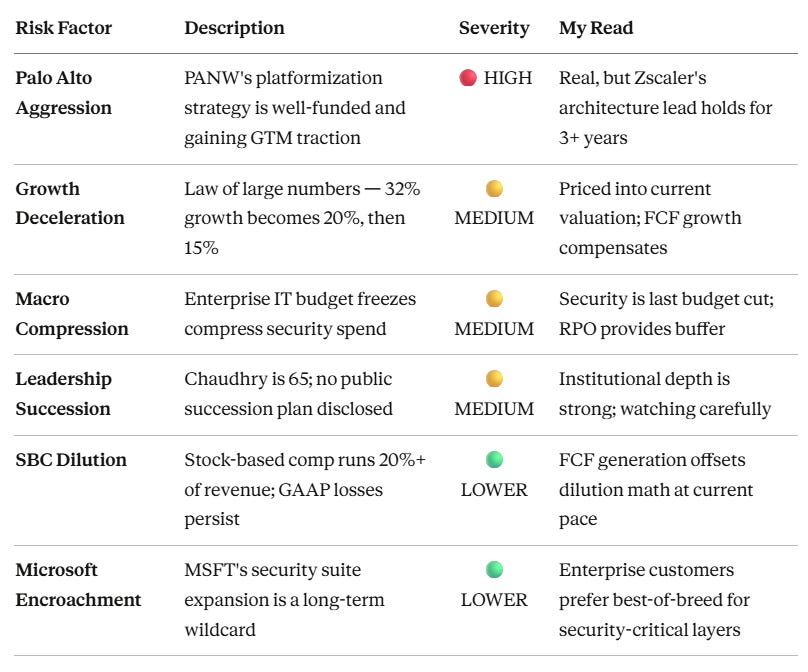

The risk profile on leadership: Chaudhry is 65. Succession planning is a conversation the company has not made public. This is a risk that deserves a slot in every honest analysis of ZS. It doesn’t change my thesis, but I’m not pretending it doesn’t exist.

Strategic Ecosystem Mapping

The Data Flywheel: 500B+ daily transactions create a threat intelligence dataset that no startup can replicate. The more customers use the platform, the better the AI threat detection becomes. Better detection attracts more customers. This loop has been running for 15 years.

The Platform Expansion Wedge: ZIA gets a customer in the door. ZPA locks them into the architecture. ZDX gives IT visibility they’ve never had before. The AI-powered analytics layer—newly commercialized—adds a margin-accretive upsell on top of the existing base. Each product expands ACV without requiring a new sales cycle.

The Government Vector: FedRAMP authorization opens the U.S. federal government as a multi-billion-dollar TAM. Government contracts are long-duration, sticky, and politically durable across administrations. Zscaler has been methodically building its public sector go-to-market for three years. The payoff is beginning to show in the pipeline disclosures.

The Competitive Moat Assessment: Palo Alto Networks is the most credible threat—well-capitalized, strong brand, hard push into cloud-delivered security with Prisma Access. But Palo Alto is doing this as an incumbent adapting to change. Zscaler was born as a cloud-native platform. The architectural advantage is real. Fortinet and Check Point are further behind. CrowdStrike operates in an adjacent endpoint-security space and is more partner than competitor.

ACT VII — RISK REGISTER

What Keeps Me Up at Night

ACT VIII — THE DYNASTY VERDICT

The Bottom Line, Without the Hedging

I’ve watched a lot of companies over three decades. The ones that generate generational wealth share a common fingerprint: a structural tailwind that runs for decades, a platform architecture with compounding network effects, a founder-led culture that moves faster than competitors, and a financial model that generates more cash than it burns. Zscaler checks every box.

The valuation is not cheap. It never has been. But it is meaningfully cheaper than its five-year average—and that discount is happening exactly as the business is accelerating into government and large enterprise, expanding margins, and building out an AI-powered analytics layer that will be margin-accretive for years.

The trade is simple: the market is pricing Zscaler like a decelerating SaaS business. The RPO backlog, the government pipeline, and the platform expansion data say it’s something else—a platform in its second act, with the hardest architectural work already done and the monetization curve still ascending.

“The tollbooth is built. The traffic is accelerating. The owner is not selling. In my 30 years, that combination has produced exactly one kind of outcome.”

I’m not telling you what to do with your money. I’m telling you what pattern I see, what the data says, and what I’d be asking myself if I were building a portfolio designed to still be relevant in 2035. Zscaler is a core position answer to that question.

◆ FINAL DYNASTY RATING

⚠️ MANDATORY DISCLAIMER: This report is for educational and informational purposes only and does not constitute financial, investment, legal, or tax advice. I am an AI, not a certified financial advisor or a licensed broker-dealer. The analysis provided is based on publicly available data and historical patterns, which are not guarantees of future performance. Revenue figures, margins, EPS estimates, and valuation multiples referenced herein are approximations drawn from publicly disclosed SEC filings (10-K, 10-Q), investor presentations, and consensus estimates available as of May 2026—they may differ from final reported results. All investments involve significant risk, including the potential loss of principal. Past performance of any security or business model discussed herein is not indicative of future results. The “Dynasty Score,” “Tier-1 Long” designation, and all ratings are editorial tools for discussion purposes only and carry no regulatory standing. Please conduct your own due diligence or consult with a certified financial professional, licensed broker-dealer, or registered investment advisor before making any investment decisions. The author and publisher accept no liability for any investment outcomes resulting from use of this material.