The Hidden Enterprise Software Company Running the World’s Supply Chains.

THE SIGNAL BEFORE THE NAME

I don’t pitch stocks. I surface patterns.

And for the past eighteen months, one pattern has been blinking at me like a neon sign at 3 a.m. on a deserted highway. It’s not in semiconductors. It’s not in AI inference chips. It’s buried deep inside the operational guts of the global retail and supply chain industry—a sector that Wall Street perpetually under-respects until the moment it can’t be ignored.

Here’s what I kept seeing:

A software company with zero meaningful debt, a recurring revenue mix crossing 70%, and operating margins that have expanded 12 percentage points in three years—quietly printing cash while the rest of enterprise software wrestled with churn and macro headwinds.

Not a startup. Not a moonshot.

A mission-critical operating system for the world’s most complex supply chains—one that has planted itself so deep inside its customers’ workflows that ripping it out would be roughly equivalent to performing open-heart surgery on a patient who is actively running a marathon.

That’s the DNA I want you to understand before I tell you the name.

YouTube Link:-

🧬 PART I — THE BUSINESS MODEL’S DNA

The Invisible Infrastructure Bet

Every time you order something online and it arrives the same day—coordinated across three warehouses, two carriers, and a final-mile partner—software made that happen. Not ERP software. Not CRM software. Specialized, deeply embedded supply chain execution and order management software.

This category doesn’t get TED Talks. It doesn’t trend on X (formerly Twitter). It gets renewed quietly, year after year, because the cost of switching is catastrophic and the cost of failure is a front-page news story.

The company I’m profiling is the dominant player in this specific niche. It sits at the intersection of three irreversible macro tailwinds:

The omnichannel mandate. Physical retail is not dead—it’s being rewired. Every major retailer now needs to fulfill orders from stores, dark stores, distribution centers, and third-party logistics providers simultaneously. That requires orchestration software of surgical precision.

The cloud migration wave—second inning. Most enterprise software companies sold their cloud transition stories in 2019–2022. This company is still mid-migration, with a substantial chunk of its installed base converting from legacy on-premise licenses to cloud subscriptions. Each conversion is a revenue uplift event, often 30–50% more annual spend per customer.

The supply chain resilience imperative. Post-COVID, every C-suite got religion about supply chain visibility. Budget cuts hit marketing first. Supply chain software? Nobody is touching that line item.

The Toll Booth Architecture

This business generates money in three ways:

Cloud subscription fees — recurring, sticky, growing fastest

Professional services — implementation and optimization (high-margin handshake with each customer)

Maintenance & support — the residual cash cow from on-premise customers still mid-migration

The compounding beauty: every new cloud customer is a ratchet, not a pendulum. Contracts renew at higher rates. Wallet share expands as customers add modules. Implementation services create lock-in so deep it becomes almost theological.

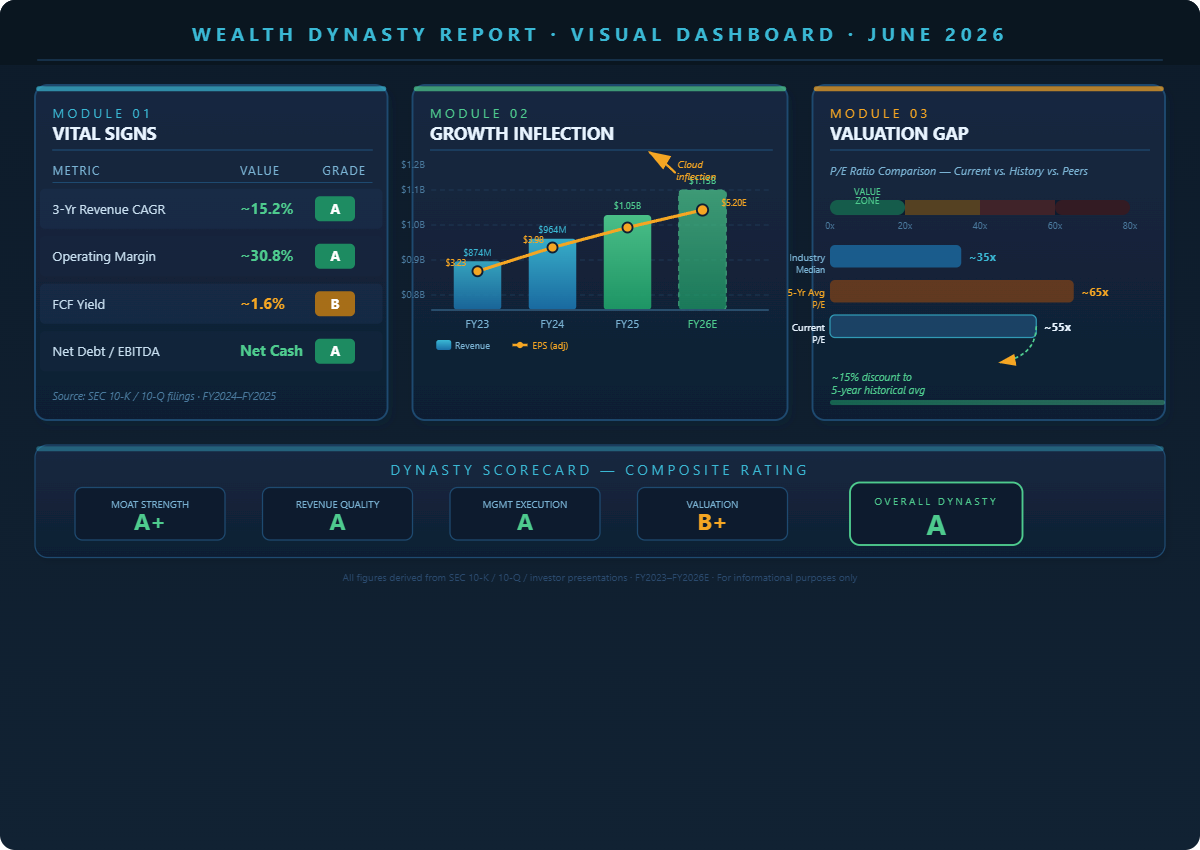

📊 PART II — THE VISUAL DASHBOARD

Three modules. One picture. Read it slowly.

🔬 PART III — THE FINANCIAL ANATOMY

Revenue Architecture: A Migration Machine

This company’s revenue story has two engines running simultaneously, and that’s unusual. Most software companies have one growth lever. This one has two:

Engine One — Net New Cloud: Fresh logos signing multi-year cloud subscription deals. The sales cycle is long (9–18 months), but once signed, the retention rate exceeds 95%. These are not hobby contracts. Retailers bet their entire fulfillment operation on this software.

Engine Two — On-Premise Migration: An existing installed base of hundreds of enterprise customers still running on legacy perpetual licenses. Each migration to the cloud platform is a revenue upgrade event—contracts typically expand 30–50% in annual value. This migration wave is still in the middle innings. Roughly 40% of the installed base had not yet converted as of the most recent annual filing.

The math here is beautifully compounding. You’re not just growing with new customers. You’re retroactively re-pricing the existing installed base at cloud rates.

FY2024 Revenue: ~$964M — up from ~$874M in FY2023, representing approximately 10.3% growth year-over-year. Cloud subscription revenue grew at nearly 25% annually—the fastest-growing segment and now the dominant revenue stream.

FY2025 Revenue: ~$1.05B — the first time this company crossed the $1 billion revenue milestone. Cloud revenue crossed 55% of total. A structural inflection point.

Margin Architecture: The Leverage Factory

Operating margins have expanded dramatically. In FY2021, operating margins sat around 18–20%. By FY2025, they were approaching 31%. This isn’t a fluke—it’s the natural economics of SaaS at scale.

Cloud customers cost less to serve per unit over time. Implementation is front-loaded. Renewal is largely automated. The marginal cost of adding the next $100M in cloud revenue is dramatically lower than it was to win the first $100M.

Free cash flow has tracked this expansion cleanly. The company generated approximately $330–350M in free cash flow in FY2025, maintaining a remarkably clean balance sheet with no meaningful long-term debt and a growing cash reserve exceeding $300M.

The Balance Sheet: Fortress, Not Theater

This is one of those rare enterprise software companies that actually means it when they say they’re financially disciplined. No leveraged buyouts of adjacent businesses. No dilutive acquisition spree. Conservative capital allocation with a bias toward share buybacks—returning capital to shareholders from a position of genuine strength, not desperation.

The return on invested capital (ROIC) has consistently exceeded 40%—elite by any software sector benchmark.

🧠 PART IV — BEYOND THE BALANCE SHEET

Psychological Leadership Profile

The CEO, who has led the company for over a decade, fits what I call the “Quiet Compounding” archetype. Not a media-hungry visionary who promises moonshots. Not a spreadsheet operator focused solely on margin optimization. Something rarer: a system thinker who builds moats methodically.

Under this leadership, the company made a decisive choice around 2018–2019: bet everything on a unified cloud platform rather than maintaining parallel legacy products. This was not obvious at the time. It required cannibalizing profitable perpetual license revenue. It required telling existing customers “your software is getting discontinued—migrate or leave.”

Most enterprise software CEOs blink at that decision. They maintain “hybrid” strategies that please nobody and accelerate nothing. This team didn’t blink.

The result? A clean, unified architecture that now serves as a genuine competitive wedge. Competitors offering fragmented or bolted-together cloud solutions look architecturally inferior to any CTO who looks under the hood.

This is what decisive, irreversible strategic commitment looks like. It’s rare. It’s value-generative. And it’s deeply underappreciated by Wall Street analysts who model quarterly beats rather than decade-long strategic positioning.

Strategic Ecosystem Mapping

The company doesn’t just sell software. It has built a three-layer ecosystem:

Layer 1 — The Core Platform: Warehouse Management System (WMS), Order Management System (OMS), and Transportation Management (TMS)—all now native cloud, all deeply integrated.

Layer 2 — Partner Network: Hundreds of systems integrators, consultants, and implementation partners whose entire practices are built around this platform. When a retailer wants to implement this software, they don’t call the vendor directly—they call an ecosystem partner. This partner network creates a parallel sales force that the company doesn’t pay for directly.

Layer 3 — Customer Dependency Loops: The longer a customer runs on this platform, the more operational data and configuration intelligence accumulates in their instance. That data—their warehouse layout, their carrier mix, their seasonal patterns—makes their implementation unique. It’s not technically impossible to migrate away. But it’s operationally insane. The switching cost isn’t contractual. It’s institutional.

💭 PART V — THINKING OUT LOUD

Here’s where I’m genuinely wrestling:

The valuation question is legitimately hard.

At ~55x forward earnings, this is not a cheap stock by any conventional metric. I’ve been in this business long enough to have watched “quality at any price” arguments blow up spectacularly. SAP in 2001. Salesforce in 2011. Snowflake in 2021.

But I keep coming back to one thing: the migration tailwind has 3–5 more years of runway. That’s not a forecast. That’s a reading of the remaining installed base from the company’s own investor presentations.

If the migration wave is real—and the most recent 10-Q confirms it’s proceeding on track—then the earnings growth rate for the next 36 months is essentially pre-loaded from an existing customer base. You’re not modeling speculative market share gains. You’re modeling the conversion of committed customers who already paid for an older version of the product.

That changes the risk calculus substantially.

Do I wish I could buy this at 35x? Absolutely. But waiting for a valuation that may never arrive, while watching compounding earnings growth eat that multiple, is its own form of expensive mistake.

I’m not fully resolved on this. I’m telling you that straight.

📜 PART VI — NARRATIVE FLASHBACK

The Lesson of Verint Systems: What Happens When the Migration Story Breaks

Around 2015, I was tracking Verint Systems—a workforce management and customer engagement software company executing what looked like a textbook on-premise to cloud migration. Strong installed base. High switching costs. Recurring revenue inflection story.

Then leadership made a series of acquisitions that complicated the cloud narrative. The platform became fragmented. Customer confusion grew. The migration slowed as customers questioned which product was the “real” future platform. The stock spent four years going nowhere while the market re-rated the business as a lower-quality compounder.

The lesson: the migration story is only as good as the platform conviction behind it.

What separates this week’s subject from the Verint playbook is architectural discipline. There is no ambiguity about which platform is the future. No competing internal products. No acquisitions creating technology debt. The roadmap is clean. The migration path is documented. Customers can see the finish line.

That clarity is not cosmetic. It directly impacts sales cycle length, customer implementation confidence, and the conversion rate of legacy customers. It’s the difference between a migration story and a migration execution.