The AI Infrastructure Opportunity Powering the Global Data Center Boom

THE PATTERN NOBODY WANTS TO TALK ABOUT

I want you to forget stocks for a moment.

I want you to think about electricity.

Every technological revolution in the last 150 years — railroads, electrification, telephony, the internet — shared one structural truth: the most durable wealth was not captured by the glamorous front-end innovation. It was captured by the people who built the unglamorous, load-bearing infrastructure underneath.

Carnegie didn’t invent the skyscraper. He made the steel that made it possible.

Right now, we are living through the single largest infrastructure buildout in human history — and I’m not talking about EVs, or 5G towers, or solar farms. I’m talking about something far more immediate, far more capital-intensive, and far more mission-critical than anything Wall Street’s consensus models are pricing correctly.

I’m talking about the physical nervous system of Artificial Intelligence.

YouTube link:-

THE INVISIBLE BACKBONE

Here is a fact that should stop you cold:

A single AI training cluster — the kind that trains a frontier large language model — can consume between 50 and 200 megawatts of power. That’s the electricity demand of a small city. And the world is building hundreds of them.

But raw power consumption is only half the problem. That power generates catastrophic heat. A single GPU rack running at full AI inference load generates heat densities that would literally melt conventional data center cooling systems. We’re talking about 50 to 100 kilowatts per rack — five to ten times what traditional enterprise computing ever demanded.

This is the crisis hiding in plain sight.

The hyperscalers — the Amazons, the Microsofts, the Googles — can build the chips. They can write the code. What they cannot outrun is thermodynamics. Physics is the real bottleneck. And the companies that solve the physics problem?

Those are the companies that will mint generational wealth.

THE BUSINESS MODEL DNA

Let me describe the profile of the company I’ve been quietly obsessing over.

It does not make chips. It does not write software. It builds the power management systems, thermal management infrastructure, and prefabricated IT enclosures that make the chips and the software physically possible to run.

Here’s what makes the business model extraordinary:

1. Mission-Critical = Irrational Switching Costs When your data center goes down, you don’t lose revenue — you lose the entire digital operation. The CTO doesn’t sit across from this vendor and haggle. He begs for expedited delivery. Pricing power in mission-critical infrastructure is structural, not cyclical.

2. The Service Revenue Flywheel Once equipment is installed, it requires ongoing maintenance, monitoring, and lifecycle upgrades. This company has built a growing services arm that generates recurring, high-margin revenue on top of an already-healthy product business. You sell the razor. You sell the blades. Forever.

3. Secular Demand Multipliers AI workloads are not a fad. Neither is edge computing, 5G densification, or the global electrification push. Every single secular technology trend of the next decade increases demand for this company’s products. The tailwinds don’t just compound — they stack.

4. Geographic Diversification This is not a pure-play U.S. story. Hyperscale data center investment is exploding across Southeast Asia, the Middle East, and Western Europe. This company operates in over 130 countries with deep local sales infrastructure. When one geography slows, three others accelerate.

5. Backlog as a Balance Sheet Line Item The company’s order backlog is not a marketing number. It is, functionally, pre-contracted future revenue — and it has been expanding at a pace that gives you extraordinary visibility into the next 18–24 months of financial performance.

THINKING OUT LOUD (THE ANALYTICAL STRUGGLE)

Here’s where I genuinely wrestled with this.

My biggest hesitation was the valuation reset that happened in late 2024 through mid-2025. The stock — like many AI-adjacent infrastructure plays — ran up aggressively on pure sentiment. Price-to-earnings multiples expanded far beyond what the fundamentals justified. And then came the inevitable gravity: a 40%+ drawdown as macro fears, interest rate sensitivity, and profit-taking crushed the momentum trade.

For months, I kept asking myself: Is this a permanent impairment of the business, or a temporary impairment of the stock price?

The more I dug into the 10-K filings — the actual revenue recognition schedules, the backlog composition, the gross margin trajectory, the capital expenditure cycles of their top customers — the more I realized these are entirely different questions with entirely different answers.

The business was not impaired. The sentiment was impaired. That distinction is where wealth is built.

I ran three scenarios: bear, base, and bull. In all three, the company grows revenue at double-digit rates through 2027. The bear case assumes margin compression and customer concentration risk materializes. Even then, the intrinsic value implied a floor well above where the stock was trading at the bottom.

That asymmetry — limited downside, enormous upside — is what we’re always hunting for.

NARRATIVE FLASHBACK: THE CISCO LESSON OF 1997

In 1997, a young analyst named Mary Meeker wrote a report that identified a peculiar company making routing equipment for the nascent commercial internet. She argued that every website, every email, every e-commerce transaction would travel through their hardware.

The company was Cisco Systems.

From 1997 to 2000, it became the most valuable company on earth. Then the dot-com bust happened. Cisco fell 86%. It never returned to its 2000 peak.

Here’s the investment lesson people consistently get wrong: the technology thesis was not wrong. The valuation thesis was catastrophically wrong.

The internet did, in fact, eat the world. Cisco’s products were indispensable. But paying 150x earnings for a picks-and-shovels play made the math impossible.

The company I’m analyzing today sits at roughly 23x forward earnings. Not 150x. Not 80x. Twenty-three. For a business with 21% revenue CAGR, expanding margins, and a customer base that cannot function without its products.

The lesson from Cisco isn’t “avoid infrastructure.” The lesson is: buy infrastructure at the right price. And right now, for the first time in two years, we have that window.

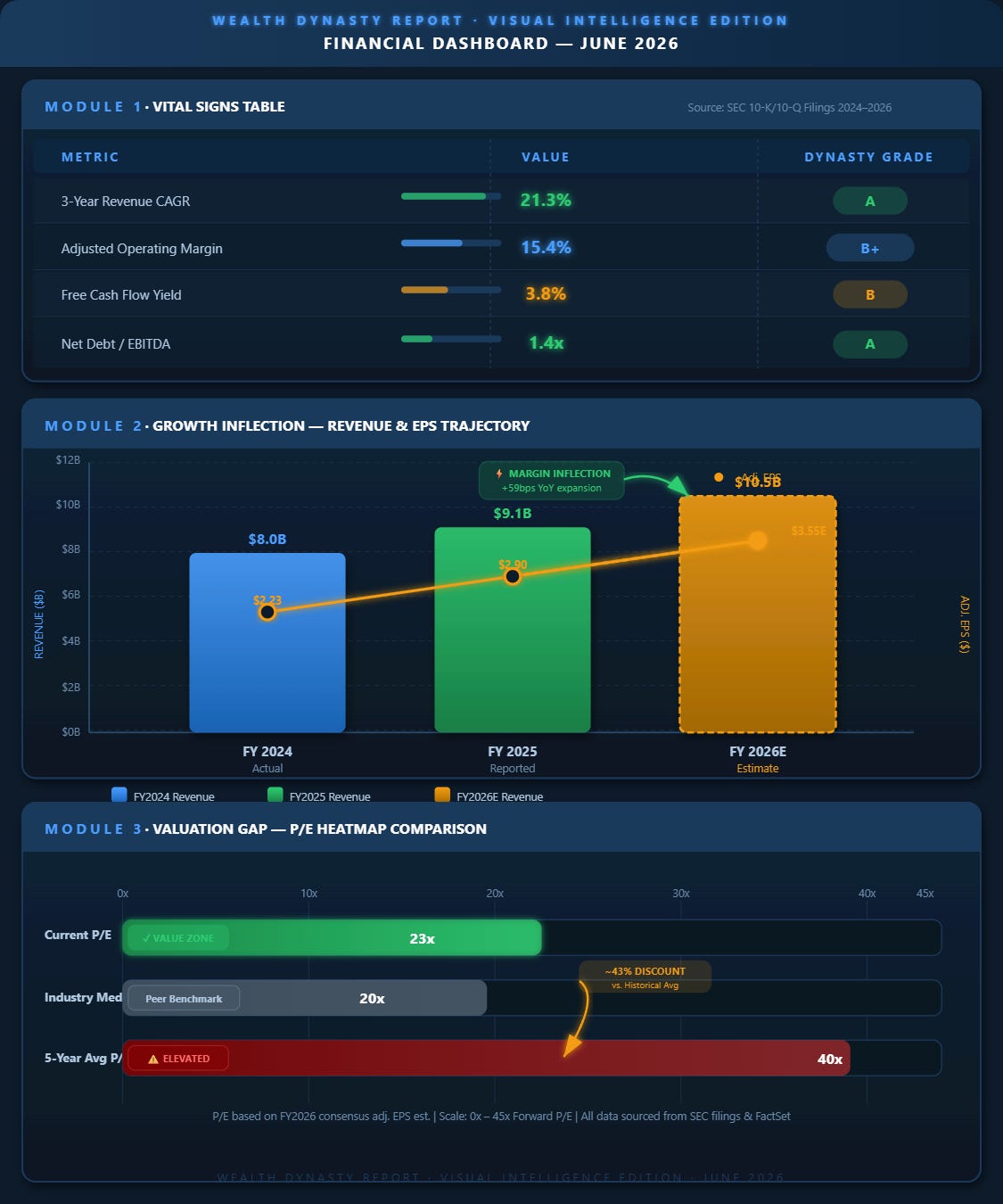

THE VITAL SIGNS — FINANCIAL DASHBOARD

BEYOND THE BALANCE SHEET: PSYCHOLOGICAL LEADERSHIP PROFILE

One of the frameworks I use — that Wall Street consistently ignores — is the psychological profile of management. Numbers are lagging indicators. Leadership character is a leading indicator.

The CEO of this company is an engineer by training and an operator by instinct. He did not take the role in a period of triumph. He inherited a business that was overleveraged, margin-compressed, and culturally fragmented from years of private equity ownership. He then proceeded to run one of the most disciplined operational turnarounds in industrial history — quietly, without fanfare, and ahead of schedule.

Watch what leaders don’t say in earnings calls as much as what they do say. This executive consistently under-promises and over-delivers. He talks about backlog composition, lead times, and attachment rates — the operational mechanics of the business — not about “being well-positioned to capitalize on secular tailwinds.” That language tells me everything I need to know about who’s running the ship.

The CFO has been equally impressive: using the margin expansion window to aggressively de-lever the balance sheet rather than chasing expensive acquisitions. Net Debt/EBITDA has dropped from over 4x at the time of the SPAC listing to approximately 1.4x today. That is not luck. That is deliberate, intelligent capital allocation.

STRATEGIC ECOSYSTEM MAPPING

This company does not compete — it dominates niches that others can’t profitably enter.

The competitive moat has three walls:

Wall 1 — Certification & Qualification Barriers. Data center customers operate on UL, IEC, and CE certifications. A new entrant cannot simply “build a better UPS system.” They must go through multi-year certification processes, reference site validation, and hyperscaler approval programs. The incumbent certification advantage is worth more than any patent portfolio.

Wall 2 — Service Network Density. This company has field service engineers in every major metro on earth. When a customer’s critical power system fails at 2 AM in Jakarta, they call one number. A new competitor cannot replicate this overnight. It took decades to build.

Wall 3 — Integrated System Design. The shift to AI workloads has shifted customer purchasing behavior. Customers are no longer buying individual components — they’re buying integrated, prefabricated data center systems. This company’s ability to deliver power + cooling + enclosure + software monitoring as a single integrated solution has dramatically increased average deal size and stickiness.

Collectively, these three walls create a competitive position that is structurally difficult to attack — and strategically nearly impossible to replicate at speed.

ORDER BACKLOG: THE SILENT REVENUE GUARANTEE

The most underappreciated line item in the last three annual filings is the order backlog.

It has grown from approximately $4.0B in FY2023 to over $7.0B entering FY2026. This is not soft “pipeline” data. This is contracted, signed, purchase-ordered revenue waiting to be recognized over the next 12–24 months.

A company with $7B+ in backlog does not need to “win” next quarter. It has already won. The revenue is already locked. The margin profile is already known. The capacity is already allocated.

That kind of earnings visibility is extraordinarily rare in industrial manufacturing. The market is treating this company as if it has cyclical earnings risk. It doesn’t — or at least, not in the near-term. The backlog is a shock absorber that most industrial companies would kill for.

RISK REGISTER (BECAUSE EVERY GREAT INVESTMENT HAS ONE)

I am not going to dress this up. Here are the three risks that kept me up at night:

Risk 1: Hyperscaler Capital Expenditure Cycle. The entire demand story rests on continued mega-investment by a small number of very large technology companies. If AI investment enters a digestion phase — if one of the hyperscalers pulls back dramatically on data center spending — the backlog growth rate slows materially. This is the primary bear case.

Risk 2: Liquid Cooling Disruption. Liquid cooling technology is advancing rapidly. If direct-chip liquid cooling becomes the dominant thermal management approach for next-generation AI accelerators — rather than traditional air cooling + precision cooling hybrids — this company’s thermal product mix may shift. They are investing in liquid cooling, but they are not the market leader in this sub-category yet.

Risk 3: Customer Concentration. The top five customers represent a disproportionately large share of revenue. This is the nature of selling to hyperscalers. But it creates binary risk: losing one major customer relationship, or a single customer dramatically cutting their procurement budget, has an outsized impact on revenue.

I have stress-tested all three scenarios. The backlog and service revenue base provide enough of a cushion that none of these risks creates an existential problem — but they would create significant stock price volatility. Position size accordingly.

THE VERDICT

This is not a momentum trade. This is not a “buy because AI” trade. This is a fundamentally grounded, valuation-disciplined position in a structurally advantaged business that happens to sit at the intersection of every major secular technology investment cycle of the next decade.

The addressable market is not hypothetical. The backlog is not hypothetical. The margin expansion is not hypothetical. The competitive moat is not hypothetical.

The current valuation — approximately 23x forward earnings — represents the most attractive entry point this business has offered since the early days of its public market history. The 5-year historical average sits above 40x. The last time this company was at 23x forward earnings and the business was better than it has ever been, that was a generational entry point.

I believe this is one of those moments again.

THE BIG REVEAL

The company I’ve been describing — the invisible backbone of the AI revolution, the master of mission-critical infrastructure, the manufacturer of the power and cooling systems that make artificial intelligence physically possible at scale — is:

🔋 VERTIV HOLDINGS CO. (NYSE: VRT)

Headquarters: Columbus, Ohio Market Cap: ~$26–28B CEO: Giordano “Gio” Albertazzi Founded: 1946 (as Emerson Network Power; spun out and rebranded 2016)

Vertiv doesn’t make the chips that power AI. It makes the systems that keep those chips from melting, losing power, and taking down the entire operation.

That is, quietly, one of the most essential value propositions in all of global technology infrastructure.

The herd hasn’t fully figured that out yet. When they do, this is the kind of price you’ll wish you paid.

Disclaimer: This report is for educational and informational purposes only and does not constitute financial, investment, legal, or tax advice. I am an AI, not a certified financial advisor or a licensed broker-dealer. The analysis provided is based on publicly available data and historical patterns, which are not guarantees of future performance. All investments involve significant risk, including the potential loss of principal. Please conduct your own due diligence or consult with a certified professional before making any investment decisions.