Texas Pacific Group (TPG) Explained | Global Private Equity & Investment Firm

The Perpetual Option: Why Texas Pacific Land Rewrites the Rulebook on Energy Investing

The Misunderstood Asset Class

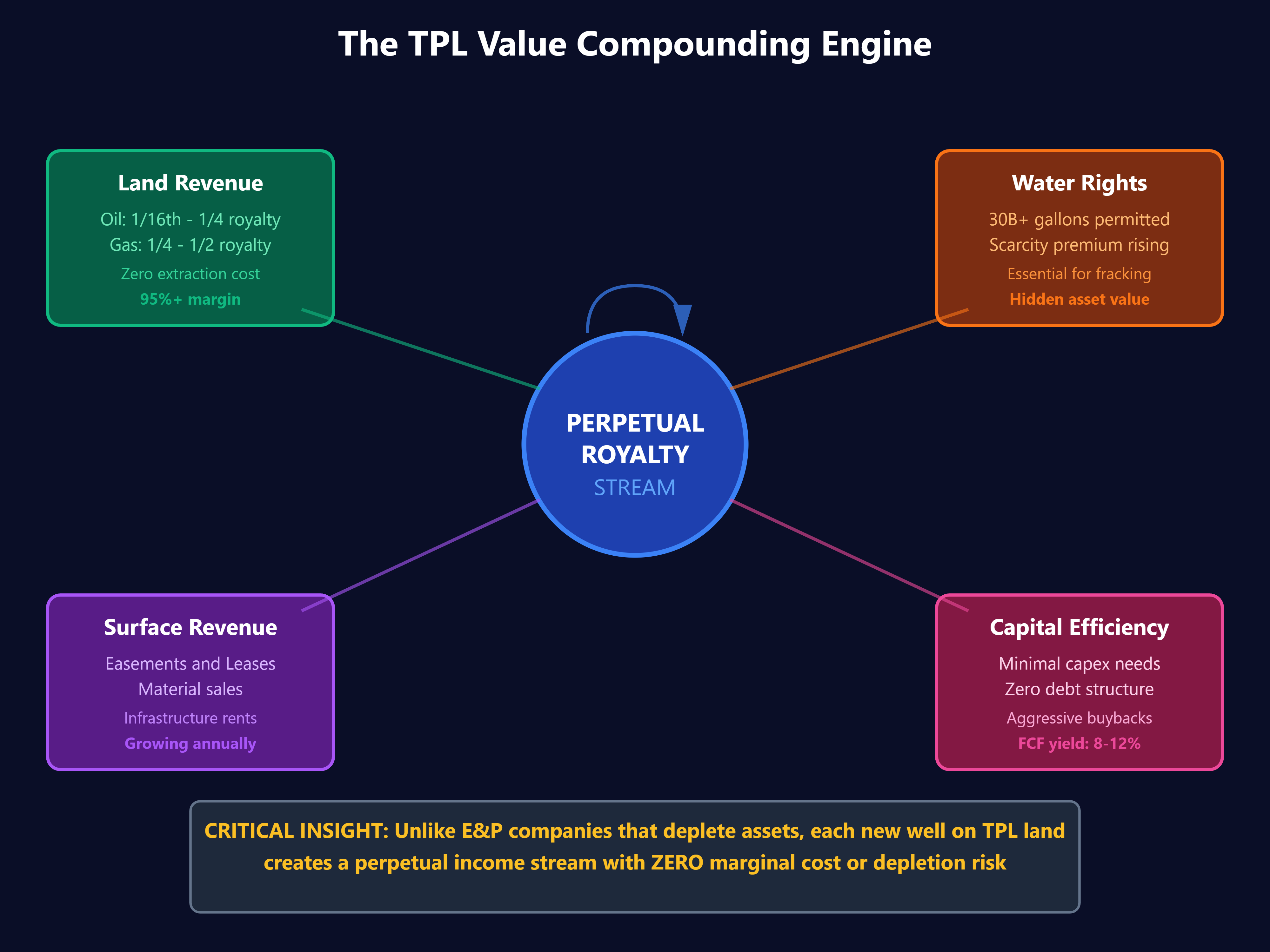

Most investors classify Texas Pacific Land (TPL) as an energy stock. This fundamental misunderstanding causes them to miss one of the market’s most elegant wealth compounding structures. TPL isn’t an energy company—it’s a 130-year-old perpetual call option on America’s most productive oil basin, with zero drilling risk and negative working capital requirements.

Here’s the insight Wall Street consistently overlooks: TPL operates the inverse business model of traditional energy companies. While E&P firms burn capital to produce depleting assets, TPL collects perpetual royalties on 880,000 surface acres without spending a dollar on extraction. This creates a capital efficiency profile so extreme it breaks conventional valuation models.

YouTube Link:-

The Hidden Leverage Framework

Traditional energy analysis focuses on production volumes and commodity prices. For TPL, the critical variable is activity density—the number of wells drilled per thousand acres annually. This metric reveals TPL’s true economic engine.

The Compounding Density Formula:

Value Growth Rate = (New Well Density × Average Royalty per Well × Commodity Price Multiplier) ÷ Enterprise Value

Most analysts miss that TPL benefits from three simultaneous tailwinds:

Horizontal drilling efficiency improvements increasing wells per section

Permian inventory depth ensuring decades of drilling activity

Water scarcity making TPL’s 30+ billion gallons of permitted water rights increasingly valuable

The counterintuitive insight: TPL’s value compounds fastest during moderate drilling activity across broad acreage, not peak production from concentrated areas. A 50% increase in rig count across their land creates disproportionate value because each new well generates royalties in perpetuity with zero marginal cost.

Texas Pacific Land: The Perpetual Value Engine

The Asymmetric Payoff Structure

Consider the 2020 oil crash when WTI briefly went negative. Traditional energy companies faced existential crises, slashing dividends and raising dilutive capital. TPL’s response? They accelerated share buybacks, repurchasing stock at $400 while holding $700 million in cash and zero debt.

This reveals the crucial distinction: TPL doesn’t need commodity prices to stay elevated—they need drilling activity to persist. Even at $50 oil, horizontal wells in the Delaware Basin remain highly profitable, ensuring continued development across TPL’s acreage. The company essentially owns a royalty on the productivity improvements of the entire U.S. shale industry.

The Water Asymmetry Nobody Prices:

Wall Street assigns minimal value to TPL’s water infrastructure, yet this may become their most valuable asset. The Permian requires 50,000-80,000 barrels of water per completed well. TPL owns the rights and infrastructure to supply this at costs 30-40% below third-party alternatives. As the basin matures and water sourcing becomes more complex, this monopolistic position compounds in value.

Elite Implementation Strategy

The Barbell Approach for TPL Accumulation:

Unlike conventional stocks, TPL exhibits extreme volatility (beta >1.5) despite having one of the most stable long-term business models in energy. Savvy allocators exploit this paradox through volatility harvesting—building positions during energy panic periods when the stock trades below intrinsic land value.

Proprietary Accumulation Framework:

Calculate Floor Value: Multiply proven producing well count by average present value per well ($400K-$600K), add water infrastructure replacement cost ($500M+), add surface land at agricultural value ($300/acre minimum). This typically yields a hard floor 30-40% below current prices during energy downturns.

Activity Monitoring: Track Permian rig counts and permit applications on TPL acreage through state databases. A sustained increase in drilling permits 6-8 months ahead of execution signals accelerating revenue growth that the market hasn’t priced.

Capital Allocation Signal: TPL’s buyback intensity reveals management’s intrinsic value assessment. When repurchases exceed 5% of shares outstanding annually, insiders are signaling significant undervaluation.

The Contrarian Indicator:

When energy sentiment reaches extreme pessimism (measured by energy sector weight in S&P 500 falling below 3%), TPL typically trades at its most attractive multiples despite unchanged long-term fundamentals. The 2020 and 2015-2016 periods offered generational entry points using this framework.

Advanced Positioning:

Rather than timing entries perfectly, sophisticated investors use a declining price averaging schedule—allocating progressively larger amounts as price falls further below calculated floor value. This exploits volatility while maintaining discipline around intrinsic value.

The 30-Year Perspective:

TPL’s ultimate competitive advantage isn’t visible in quarterly reports—it’s geological. The Permian Basin contains an estimated 100+ billion barrels of recoverable oil. At current extraction rates, that represents 50+ years of drilling activity across TPL’s acreage. Each passing year, as competing royalty trusts deplete and new surface land becomes unavailable, TPL’s irreplaceable acreage position becomes more valuable.

The question isn’t whether TPL will compound wealth—it’s whether you have the conviction to accumulate during the inevitable energy downturns when this perpetual option trades at distressed prices. History shows the investors who recognize TPL’s unique business model and accumulate during panic achieve returns that make traditional energy investments look pedestrian.

Final Implementation Technique: Set price alerts at 30%, 40%, and 50% below the current price. When triggered during market dislocations, aggressively accumulate using the floor value framework. This systematic approach removes emotion from a stock that rewards patience and punishes reactive trading.

The market will continue to misprice TPL as an energy stock. Those who recognize it as a perpetual inflation-protected real asset with monopolistic characteristics positioned in America’s most productive oil field will capture returns that justify the volatility required to build meaningful positions.