🔍 IonQ, Inc. — Research Report

June 20, 2026 · US Markets · CMP: $56.55

Investment Thesis

IonQ represents a high-risk, high-reward bet on the foundational shift to quantum computing. The core thesis posits that IonQ’s trapped-ion technology positions it as a leading contender in a nascent, transformative industry, capable of delivering exponential computational advantages. While the company exhibits strong revenue growth from a low base, the current valuation reflects future potential far removed from present operational realities.

Competitive Edge & Growth Driver

IonQ’s competitive edge is anchored in its trapped-ion quantum computing architecture, which consistently demonstrates high qubit fidelity and connectivity, essential for building more reliable and powerful quantum systems. Its modular design and cloud-agnostic approach further enhance accessibility and scalability for developers and enterprises. The most critical growth driver over the next 12–18 months will be achieving a clear milestone in error-corrected qubits or demonstrating a “quantum advantage” for a specific, commercially viable application, thereby accelerating adoption among early enterprise customers in areas like materials science or complex optimization problems. Continued expansion of cloud partnerships and government contracts will be key indicators of this momentum.

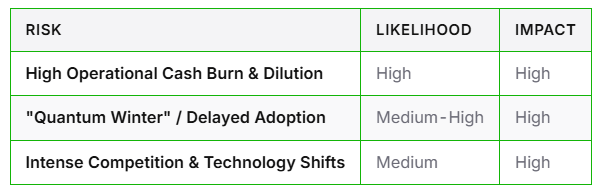

Key Risks

Valuation & Recommendation

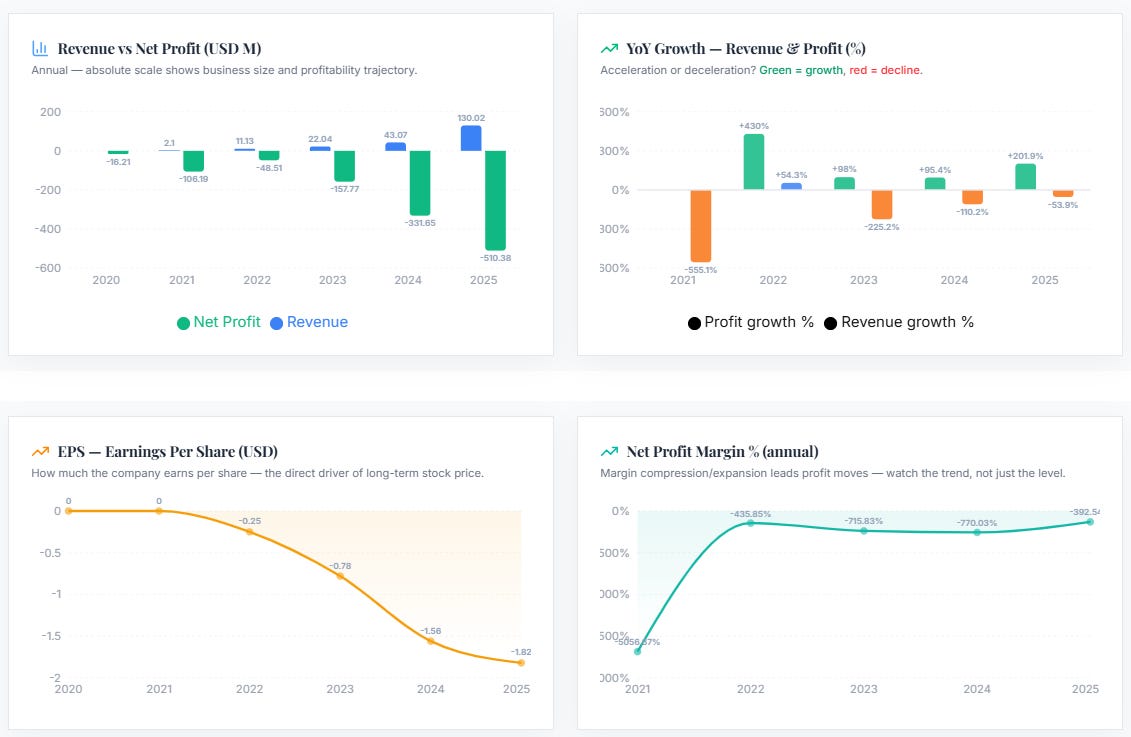

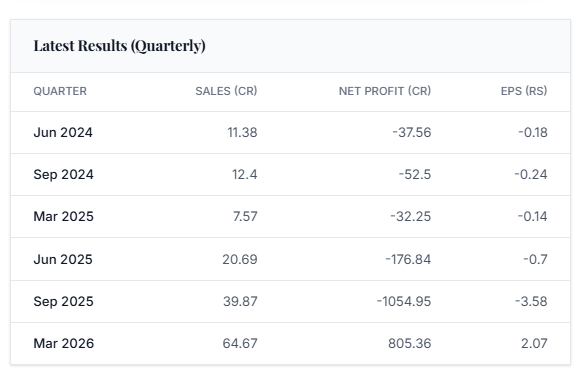

We believe P/Sales is the most appropriate valuation metric given XXXX’s deeply negative operating and net margins, rendering traditional earnings or cash flow multiples uninformative. While sales growth is robust, the company’s LTM operating margin of -487.39% and net margin of -392.54% highlight a severe operational cash burn. The positive net profit reported in March 2026, juxtaposed with significantly negative EBITDA in the same period, suggests a non-recurring, non-operational gain that does not reflect an improvement in core profitability.

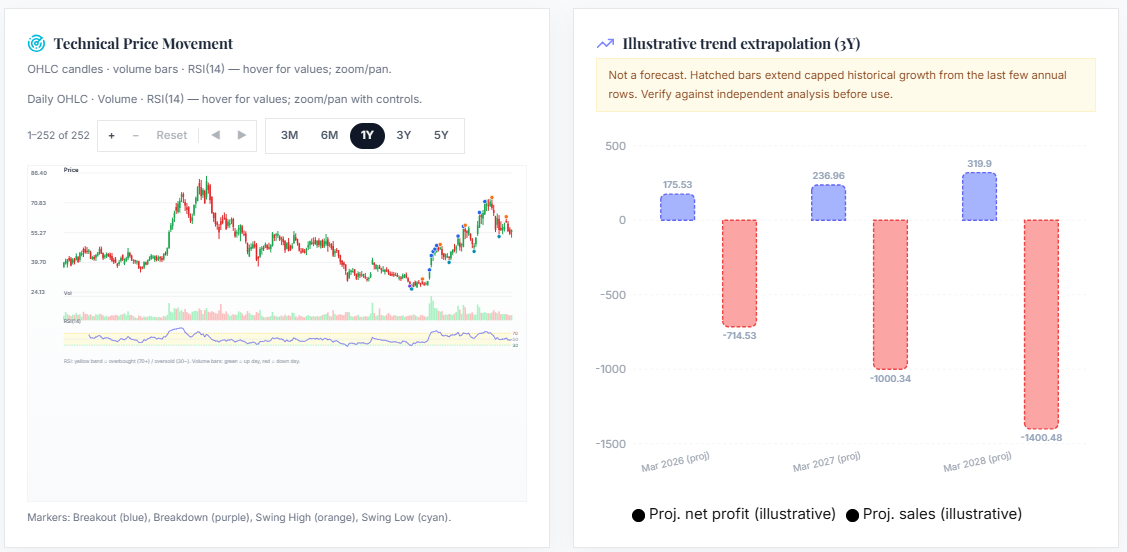

Our 12-month target price is USD 35.00, based on a forward P/Sales multiple of 28x applied to our estimated 12-month forward sales of USD 250 million. This multiple, while still generous for a deeply unprofitable company, represents a significant rationalization from the current LTM P/Sales multiple (approx. 85x).

Implied Upside: ((35.00 − 56.55) / 56.55) × 100 = -38.11%

Recommendation: AVOID — Current valuation significantly overstates the near-term commercialization prospects and underestimates the persistent operational losses and likely future dilution requirements.

📊 Financial Performance

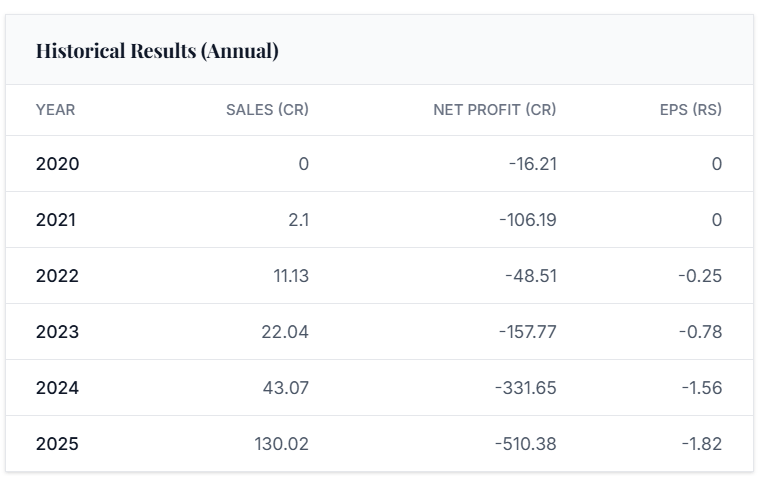

Annual Results

Quarterly Results (recent)

🔓 Company Reveal — Subscribers Only

Company : IonQ, Inc.

Ticker : IONQ Exchange SEC Current Price $56.55 Research View on Nasdaq.com

This research is for informational purposes only and does not constitute investment advice.