GitLab (GTLB) Stock : Growth Potential, Risks & Long-Term Investment Outlook (2026 Edition)

I. The Pattern That Keeps Printing Money

There is a specific type of infrastructure company that gets built maybe once per technology cycle. Not an app. Not a consumer product. Not another ChatGPT wrapper. I mean the kind of company that sits directly inside enterprise workflows — embedded so deep that ripping it out would require shutting down software development itself. These companies share a fingerprint: high switching costs baked into daily operational DNA, gross margins that look more like a toll booth than a factory, and a customer base that doesn’t churn — it compounds.

The pattern appeared in the 1990s with database vendors. It appeared again in the 2000s with ERP systems. In the 2010s, it was cloud infrastructure. Right now, in 2026, the pattern is crystallizing around the software development lifecycle — and one company has quietly become the operating system for how enterprises actually build, test, secure, and ship code.

Here’s what makes the DNA so distinctive: they do not sell you a feature. They sell you an entire workflow. Planning, coding, testing, security scanning, deployment, monitoring — all inside a single platform. The moment an enterprise standardizes on this approach, every developer’s daily ritual runs through this system. Pull requests. Code reviews. CI/CD pipelines. Vulnerability scans. Compliance audits. The productivity and security machinery of a modern software organization all funneling through one platform.

⚙ Business Model DNA

The “Platform Trap” Dynamic: When developers store years of code history, CI/CD configurations, security rules, and compliance policies in one platform, migration cost isn’t just financial — it’s organizational. Every new developer hired learns the platform first. The moat deepens with every commit pushed.

YouTube Link:-

II. The Industry Dislocation Nobody Is Talking About

There’s a fundamental shift happening in enterprise software that Wall Street analysts are processing incorrectly. They see AI code assistants and panic: “Won’t AI make developers obsolete? Won’t this destroy demand for dev tools?” This reasoning is exactly backwards.

When AI generates more code — and it is generating dramatically more code — you don’t need less infrastructure to manage that code. You need more. More testing. More security scanning. More governance. More compliance checking. More deployment pipelines. Code volume is exploding, and that explosion is a tailwind, not a headwind, for the platform managing it all.

Think about this: if an AI agent writes 10x more code per developer, every line of that code still needs to pass through version control, get reviewed, get security-scanned for vulnerabilities, and get deployed. The workflow management platform becomes more critical, not less.

📜 Narrative Flashback · 2003

When email volume exploded in corporate America during the early 2000s, skeptics asked: “Won’t all this email destroy the need for Microsoft Exchange?” The opposite happened. Exchange became irreplaceable infrastructure. Microsoft’s server revenue compounded for a decade as email became the nervous system of enterprise communication. The platform that manages a communication channel does not suffer when that channel grows — it wins. The analogy to code infrastructure today is almost uncomfortably clean.

III. The Financial Architecture: Reading the Real Signal

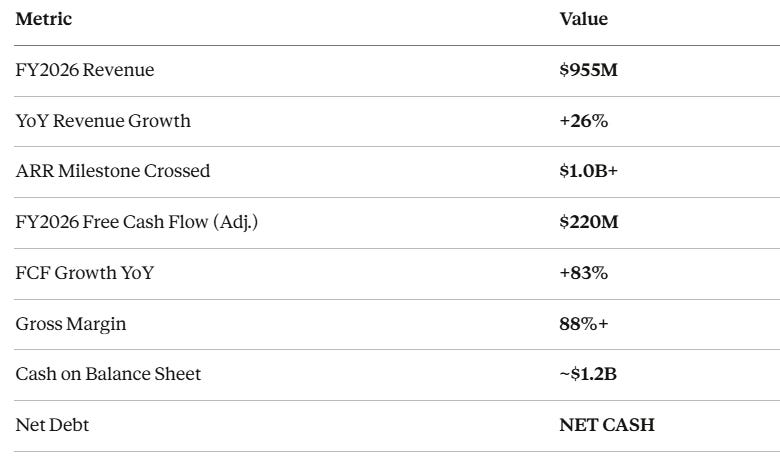

This company’s gross margins sit at 88%+. Let that land. On every additional dollar of subscription revenue, they retain 88 cents before a single R&D or sales dollar gets spent. This is not a software company trying to be a SaaS company. This is the genuine article — a subscription model with near-zero marginal cost for existing customers.

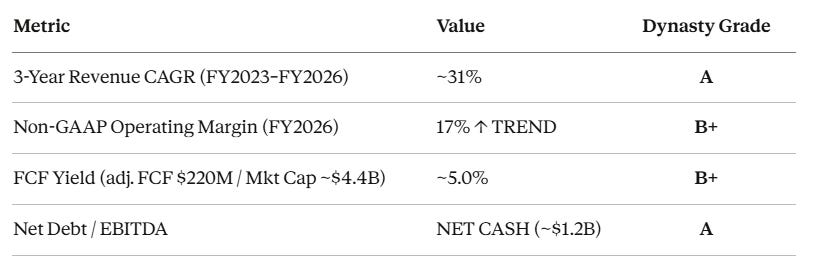

The revenue trajectory is equally striking. Over the past three fiscal years ending January 2026, they’ve compounded revenue at roughly 31% annually — growing from ~$424M in FY2023 to $955M in FY2026. That kind of sustained top-line momentum at this scale is rare. Most companies at $1B in revenue are lucky to grow 15%.

Key Financial Metrics at a Glance

But here’s what makes FY2026 a genuine inflection point: free cash flow exploded. $220 million in adjusted FCF — up 83% year-over-year with over seven points of FCF margin expansion. This is not accounting noise. The business crossed the threshold from cash consumer to cash machine, and that transition is almost always when institutional investors wake up to a stock that retail has been sleeping on.

🤔 Thinking Out Loud — An Analytical Struggle

Here’s where I genuinely wrestle with this name. The company’s Dollar-Based Net Retention Rate has been drifting down — a real crack in the foundation that I can’t paper over. Management acknowledged that bookings growth has not kept pace with reported revenue for three years. Price-sensitive customer segments, particularly in the public sector, are compressing expansion rates. The ratable revenue recognition model means today’s booking weakness flows into tomorrow’s revenue with a lag. So am I early on the inflection — or am I catching a falling knife at a lower altitude?

My resolution: the $220M FCF proves the business is real and structurally sound. The $400M buyback authorization proves management has conviction. And the $1.0B ARR milestone proves retention at the enterprise tier is holding. The mid-market churn concern is real, but the thesis doesn’t live or die in that cohort.

IV. The Customer Fortress: Where The Real Moat Lives

The company now has 1,456 customers paying over $100,000 annually — up 18% year-over-year, representing over 75% of total ARR. More strikingly, the cohort of customers spending over $1 million per year surpassed 155 customers, growing 26% — the largest such cohort in company history.

The mix matters enormously here. When a company the size of Volkswagen Digital Solutions, NatWest, or Highmark Health bets its entire software development workflow on this platform, that contract is not renewed quarterly on a whim. It’s renewed because the cost of switching — retraining every developer, migrating years of CI/CD pipelines, rebuilding security compliance workflows — far exceeds any conceivable savings from moving to a competitor.

Over 50% of the Fortune 100 now trusts this platform. That’s not a marketing slide. That’s competitive insulation.

⬡ Visual Intelligence Dashboard

Three-Module Analysis · Based on SEC Filings FY2024–FY2026

MODULE 01 · VITAL SIGNS

Sources: GitLab 10-K FY2026 (Filed March 2026, SEC Accession); Q4 FY2026 8-K Earnings Press Release March 3, 2026. Non-GAAP figures as defined by company.

MODULE 02 · GROWTH INFLECTION — REVENUE & FCF TRAJECTORY

Revenue ($M) Adj. FCF ($M)

─────────────────────────────────────────────────────────────────

$955M ┤ ████ ◄── FCF INFLECTION

│ ████ +83% YoY · $220M

$800M ┤ ████ ●

│ ████ ████ /

$700M ┤ ████ ████ /

│ ████ ████ / $120M

$600M ┤ ████ ████ ████/

│ ████ ████ ████

$500M ┤ ████ ████ ████

│ $580M ████ ████ ████ $23M

$400M ┤ ████ $759M████ ████ ●

└──────────┬───────────┬────────┬──────────────────────────

FY2024 FY2025 FY2026 (ACTUAL 10-K)

Jan 2024 Jan 2025 Jan 2026

■ Revenue (bars) ● —— Adj. Free Cash Flow (line)

■■■ (darker green) = FY2026 Actual per 10-K

Key Reading: The orange FCF line tells the real story — from $23M → $120M → $220M. The business didn’t just grow revenue; it crossed the structural threshold from cash consumer to cash generator. That transition reprices multiples.

MODULE 03 · VALUATION GAP — EV/REVENUE HEATMAP

0× 4× 8× 12×

│ │ │ │

Current ██████ 3.6× ◄── ✦ VALUE ZONE (Green)

5-Yr Average ████████████████████████████████████ 12×

Industry Med ██████████████████ 7×

─────────────────────────────────────────────────────────────────

Current ████ 3.6× ← 70% below own historical average

5-Yr Avg ████ 12.0× (estimated from 2021–2025 pricing data)

Ind. Median ████ 7.0× (DDOG, HUBS, MDB, ESTC peer set)

Stock trades at a 70% discount to its own historical average — at a moment when FCF is at record highs. That gap is the opportunity.

Sources: Yahoo Finance (March 2026 data); GitLab 10-K FY2026; industry comp set = DDOG, HUBS, MDB, ESTC. Historical average estimated from public pricing data 2021–2025.

V. Beyond the Balance Sheet: Leadership Psychology & Strategic Ecosystem

The Psychological Profile of Bill Staples (CEO)

Staples joined as CEO in 2022 — a critical hire because GitLab needed to transition from visionary founder-led scrappiness to disciplined enterprise execution. His background at Microsoft and New Relic gives him the DNA of someone who knows how to expand inside large enterprise accounts rather than just land-and-celebrate. The language he uses on earnings calls is instructive: “More code means more of a need for GitLab” — a calm, structural argument rather than a hype cycle pitch. This is the voice of a CEO who knows his industry tailwind is structural, not cyclical.

What concerns me about his profile: the company has not solved its pricing segmentation problem elegantly. Price-sensitive customers — particularly smaller public-sector accounts — are churning or downtiering. A truly elite enterprise CEO would have already built a tiered product architecture that captures both cohorts. The Duo Agent Platform’s new usage-based “GitLab Credits” pricing model is the right structural response, but it came late.

The Strategic Ecosystem Map: Who They Sit Between

GitLab occupies a specific strategic chokepoint. On the left side sits the AI code generation layer — GitHub Copilot, Cursor, Amazon Q, Anthropic Claude Code. On the right side sits the deployment and observability layer — Datadog, Dynatrace, HashiCorp. GitLab is the orchestration platform in the middle, the place where code generated by AI assistants gets validated, secured, and shipped.

Critically, GitLab is integrating with competitors rather than fighting them — their Duo Agent Platform works with Claude Code, OpenAI Codex, and Google Gemini CLI directly. This is a masterclass in ecosystem strategy: become the plumbing that all the exciting new tools flow through.

The $400 million buyback authorization announced on March 3, 2026 signals something important strategically: management is not chasing expensive acquisitions right now. They’re confident enough in organic compounding to buy the cheapest asset they own — their own stock at $26.

VI. The Honest Risk Register

Net Retention Drift: Dollar-Based Net Retention has been sliding for several quarters. When existing customers expand more slowly, future revenue becomes a function of new logos — a more expensive, less predictable growth engine. This is not fatal, but it’s a genuine margin of safety concern.

GitHub’s Microsoft Muscle: Microsoft has unlimited distribution through GitHub and enterprise Azure relationships. They can bundle GitHub Copilot, GitHub Actions, and Azure DevOps in ways that make individual pricing comparisons meaningless. GitLab’s answer — superior security integration and a single platform versus Microsoft’s patchwork of tools — is the right one, but enterprise IT budgets are political.

Agentic AI Revenue Timeline: The Duo Agent Platform is the right product for the AI-native development world. But management explicitly cautioned that revenue contribution will be modest in FY2027 due to adoption cycles. Investors expecting an immediate revenue bump from AI will be disappointed. This is a FY2028 and beyond story.

FY2027 Guidance Was Sobering: Management guided FY2027 revenue to $1.10B–$1.12B — only ~16% growth, a step-down from FY2026’s 26%. The stock’s reaction (down ~2.6% after beating earnings) reflects the market’s unease with decelerating topline momentum even as margins and FCF expand. If you need near-term multiple re-rating from revenue acceleration, this is not your trade.

Dynasty Verdict

Dynasty Rating: B+ · Accumulate on Weakness

3.6× EV/Revenue at $220M FCF is structurally cheap. The AI orchestration thesis is correct and durable. Position size to the risk: net retention headwinds and growth deceleration are real. This is a 3-to-5 year compounding position, not a Q2 trade.

VII. The Dynasty Thesis in Three Sentences

GitLab (NASDAQ: GTLB) is the infrastructure backbone of enterprise software development — a $955M revenue machine with 88%+ gross margins that just generated $220M in free cash flow, crossed $1 billion in ARR, and is trading at 3.6× EV/Revenue while its five-year historical average was 12×. The company sits at the chokepoint where every line of AI-generated code must pass for security, compliance, and deployment — making it a structural beneficiary, not a casualty, of the AI code explosion. At $26 per share with a $400M buyback and a net cash balance sheet, the downside is bounded; the upside depends on whether Duo Agent Platform delivers the monetization management is promising for FY2028 and beyond.

DISCLAIMER: This report is for educational and informational purposes only and does not constitute financial, investment, legal, or tax advice. I am an AI, not a certified financial advisor or a licensed broker-dealer. The analysis provided is based on publicly available data including GitLab Inc. SEC filings (10-K FY2026, 8-K dated March 3, 2026), official earnings press releases, and publicly available exchange data, which are not guarantees of future performance. Financial figures are sourced from official filings and investor relations materials; estimated or derived figures are explicitly noted. All investments involve significant risk, including the potential loss of principal. Past performance and historical patterns are not indicative of future results. The views expressed represent analytical interpretation only. Please conduct your own due diligence or consult with a certified financial professional before making any investment decisions. GitLab Inc. (NASDAQ: GTLB) is a publicly traded company; the author of this report holds no positions and receives no compensation from any company mentioned.