Dividend Analysis: Beyond the Obvious Metrics

Paradigm-Shifting Insight Introduction

Most investors, even seasoned professionals, fall prey to the Siren’s song of high dividend yield. They chase the highest percentages, believing it signifies immediate value. This is a profound misunderstanding. High dividend yield, particularly in a static or declining business, is often a value trap – a symptom of a distressed stock price, not a robust income stream. The truly exceptional dividend opportunities, the ones that build generational wealth, often present with moderate or even low initial yields but possess an “invisible” growth trajectory that Wall Street largely misses.

For a visual walkthrough of this story, check out the full video here

Youtube Link:

The Illusion of High Yield & The Power of “Invisible” Growth

Traditional analysis fixates on yield and payout ratio as isolated metrics. The genuine alpha lies in their interplay with a company’s Sustainable Dividend Growth Rate (SDGR), a metric rarely discussed in mainstream reports. This isn’t just about earnings growth; it’s about the organic capacity of a business to increase dividends year after year without compromising future growth or financial stability. Ignoring this dynamic means you’re investing in the rearview mirror, not the road ahead.

Advanced Analytical Framework: The “Dividend Longevity Quotient” (DLQ)

My proprietary Dividend Longevity Quotient (DLQ) moves beyond static ratios to assess the true sustainability and future growth potential of a company’s dividend. It’s a multi-factor assessment, but at its core, it combines:

Adjusted Payout Ratio (APR): Instead of just earnings, we use Free Cash Flow (FCF) Payout Ratio, adjusting for non-recurring items and CapEx cycles. A healthy APR should ideally be below 60% for mature companies and even lower (30-40%) for growth-oriented dividend payers, allowing for reinvestment. Anything consistently above 80% (even if earnings-based looks fine) signals caution.

FCF Growth Momentum (FCF-GM): This isn’t just historical FCF growth. It’s about analyzing the drivers of FCF growth over the last 5-7 years. Is it through market share gains, new product cycles, cost efficiencies, or purely cyclical tailwinds? We look for structural, defensible sources of FCF growth, not just ephemeral ones. This involves deep dives into industry dynamics and competitive moats.

Return on Invested Capital (ROIC) vs. Cost of Capital (CoC) Spread: A company’s ability to consistently generate ROIC significantly above its CoC is paramount. This spread indicates superior capital allocation and the potential to reinvest retained earnings at high rates, which fuels future dividend growth without excessive debt. A widening spread is a powerful bullish signal for dividend longevity.

DLQ Scorecard (Simplified):

High DLQ: APR < 50%, FCF-GM > 10% (driven by structural factors), ROIC-CoC Spread > 5%. (Exceptional dividend compounders)

Medium DLQ: APR 50-70%, FCF-GM 5-10%, ROIC-CoC Spread 2-5%. (Reliable dividend payers, some growth potential)

Low DLQ: APR > 70%, FCF-GM < 5% or declining, ROIC-CoC Spread < 2%. (Potential value traps, unsustainable dividends)

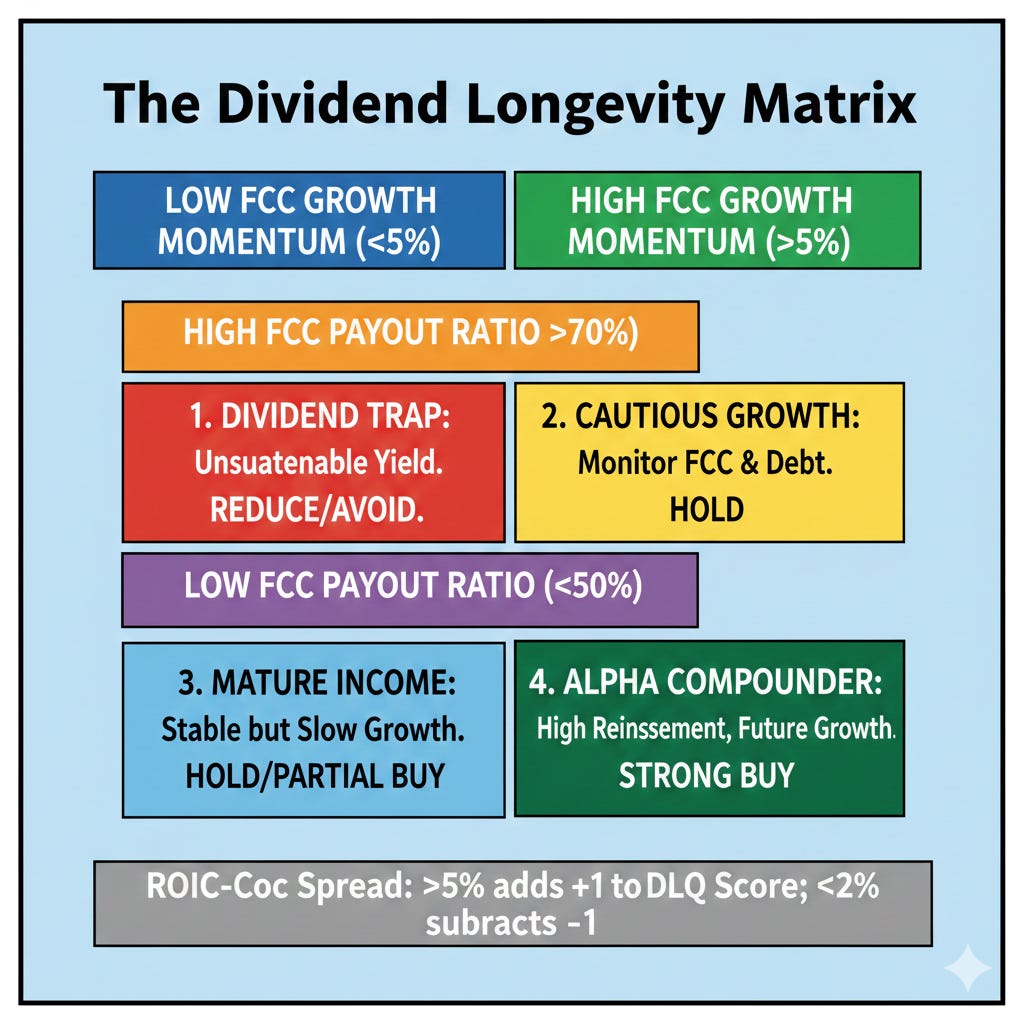

Visual Knowledge Synthesis: The Dividend Longevity Matrix

This matrix visually synthesizes the core components of the DLQ, guiding your decision-making beyond superficial yield.

Elite-Level Application Examples:

Case Study 1: Hindustan Unilever (HUL) - The Alpha Compounder (Quadrant 4) For years, HUL might have appeared to offer a modest dividend yield. However, a deeper dive using the DLQ reveals its true power. Its Adjusted Payout Ratio (FCF basis) has consistently been managed efficiently, typically in the 60-70% range. Crucially, its FCF Growth Momentum, driven by category leadership, brand power, and effective cost management in the vast Indian consumer market, has been robust and structural. Most importantly, HUL’s ROIC has consistently remained significantly above its CoC, signifying superior capital allocation and a powerful engine for reinvestment that fuels future dividend increases. While not a “high yield” stock, its consistent, predictable dividend growth combined with capital appreciation from sound business fundamentals makes it a true generational wealth builder.

Case Study 2: Select PSUs (Public Sector Undertakings) - The Dividend Trap (Quadrant 1) Many PSUs often boast seemingly attractive high dividend yields. However, our DLQ analysis frequently flags them as dividend traps. Their high payout ratios (often mandated by government ownership) frequently exceed their sustainable FCF generation. FCF Growth Momentum is often stagnant or reliant on government contracts rather than organic market expansion. The ROIC-CoC spread is often thin or even negative, indicating inefficient capital deployment. Investors chasing these yields often find their capital eroding as the underlying business stagnates or declines, illustrating that a high yield alone is not a proxy for quality.

Implementation Strategy: The “Growth-First Dividend Portfolio”

Instead of building a portfolio around current yield, focus on a “Growth-First Dividend Portfolio” strategy:

Screen for DLQ: Prioritize companies with a strong or improving DLQ score, emphasizing those in Quadrant 4 of our matrix. Look for sustainable FCF growth drivers and a healthy ROIC-CoC spread.

Ignore Initial Yield Bias: Don’t be swayed by low initial yields if the DLQ is strong. A company yielding 1.5% today but growing its dividend by 15% annually will soon outperform a 5% yielder with 2% growth.

Monitor Payout Trends: Continuously track the FCF Payout Ratio. A sudden, significant increase without a corresponding increase in FCF-GM or a solid explanation is a red flag.

Reinvestment Discipline: For younger investors, consider reinvesting dividends from these “Alpha Compounders.” The compounding effect of growing dividends reinvested into a growing business is profoundly powerful over decades.

Look for “Invisible Growth”: Seek out companies investing heavily in R&D or market expansion that might temporarily suppress current FCF but lay the groundwork for accelerated FCF and dividend growth in the future. These are often overlooked gems.

By shifting your focus from the immediate gratification of high yield to the long-term compounding power of sustainable dividend growth, driven by robust free cash flow and intelligent capital allocation, you unlock a hidden layer of alpha that most of the market simply misses. This is how generational wealth is built, one intelligently selected dividend at a time.