Check Point Software Technologies (NASDAQ: CHKP)

Working Capital & Liquidity Deep-Dive

SECTION I: Investment Thesis & Summary

Check Point is one of the most profitable cybersecurity companies on the planet, and right now it’s sitting at its cheapest valuation in years. The stock is down roughly 27% from its 52-week high of $234 — not because the business is broken, but because the market is nervous about one thing: growth. Wall Street wants 15% revenue growth and Check Point keeps delivering 6%. That’s the whole story. If you’re patient, this is a company with a fortress balance sheet, $4.3 billion in cash and securities, and a machine that prints over $1.2 billion in operating cash every year.

YouTube Link:-

SECTION II: Business Model & Operations

Check Point is an Israeli-headquartered cybersecurity giant that’s been doing this since 1993. They protect over 100,000 organizations around the world — governments, banks, hospitals, Fortune 500 companies — from hackers, ransomware, and data theft. Think of them as the original cybersecurity company that never stopped evolving.

The way they make money is elegant. Three buckets:

First, they sell physical hardware appliances — these are the actual security gateways that sit at the edge of corporate networks. That business brought in about $548M in FY2025. Second, and this is the exciting one, they sell cloud-based security subscriptions through their Infinity Platform. That’s $1.22 billion in FY2025 and growing 10% a year. Third, they lock in recurring software maintenance and support revenue — another $958M — which is sticky like glue because nobody wants to switch their security provider mid-year.

Geographically, about 50% of revenue comes from Europe, Middle East, and Africa. The Americas contribute around 40%, and Asia-Pacific rounds it out at about 10%.

The big shift happening right now is management’s push into AI-powered security. They’re not just building firewalls anymore. In 2025 alone, they acquired Cyberint (threat intelligence), Lakera AI (AI security for agentic applications), and three more companies in early 2026 — Cyata, Cyclops, and Rotate. This is a company actively reinventing itself for the AI era of cyber threats. Their new CEO, Nadav Zafrir, took over in 2024 and has been crystal clear: the strategy is to be the company that secures AI infrastructure, not just traditional networks.

SECTION III: Historical Financial Review

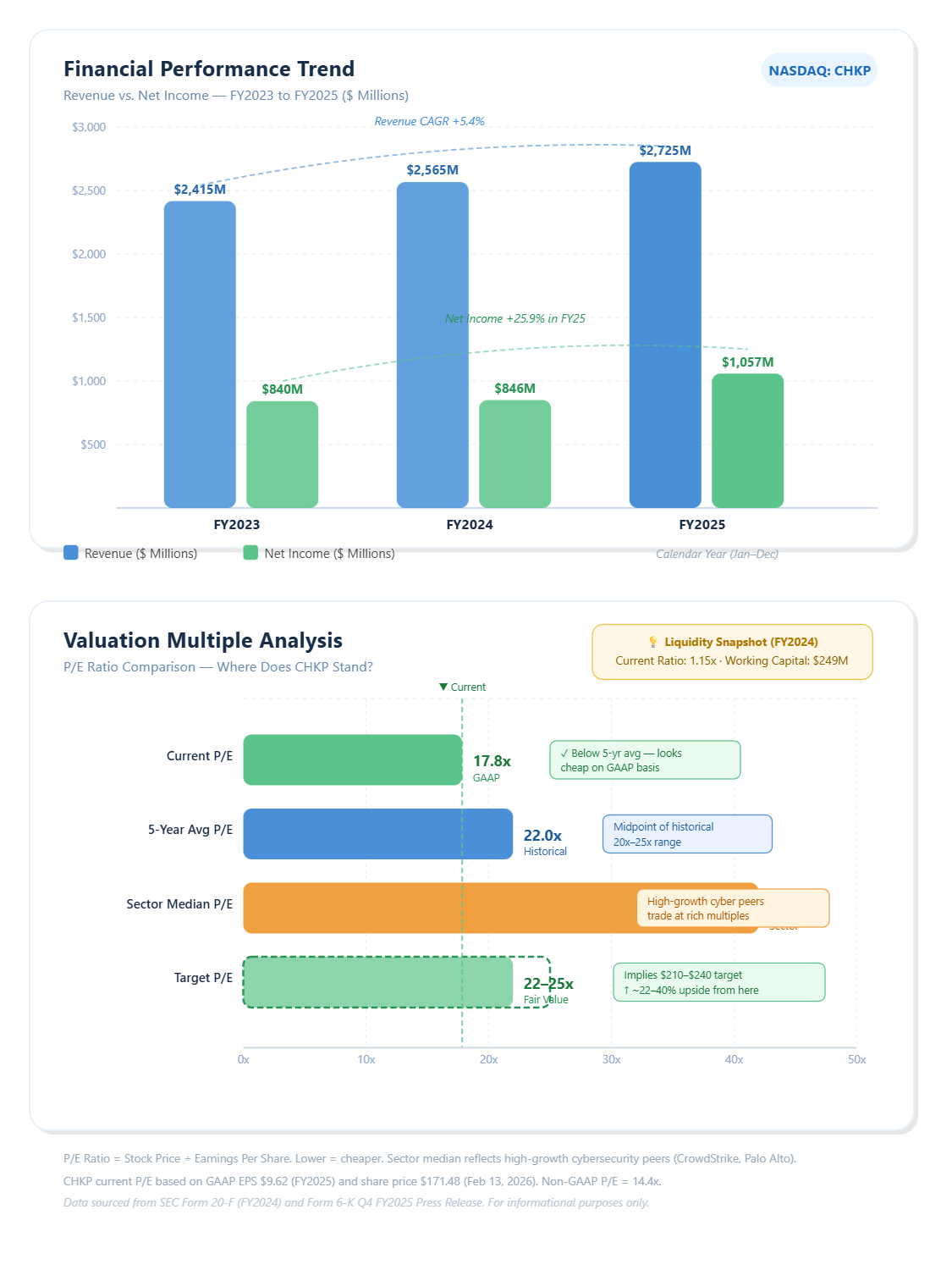

Let’s look at the three-year revenue story. In FY2023 (calendar year ending December 2023), Check Point pulled in $2.41B in revenue. In FY2024, that grew to $2.57B. And in FY2025, they hit $2.73B. That’s a three-year revenue CAGR of about 5.4%. Steady, not spectacular.

But here’s where it gets interesting — the profit story is far stronger than the revenue story.

GAAP net income jumped from around $840M in FY2024 to over $1.06B in FY2025. That’s a 25% earnings jump on just 6% revenue growth. How? Two things. First, the company got a big tax benefit from settling some prior-year Israeli tax disputes — which added roughly $1.90 to EPS. Second, their subscription revenue mix is improving, and subscriptions carry higher margins than hardware. Even stripping out the tax benefit, underlying earnings growth was healthy at around 15%.

Full-year GAAP EPS came in at $9.62 for FY2025, up from $7.46 in FY2024. Non-GAAP EPS — which strips out stock compensation and acquisition costs — hit $11.89.

On cash, they are sitting on something extraordinary. As of December 31, 2025, Check Point had $4.34 billion in cash, marketable securities, and short-term deposits. That’s up from $2.78B a year earlier. The big jump? They raised $2 billion through a convertible notes offering in December 2025. This is new long-term debt — the first time Check Point has meaningfully levered up in years. They used part of the proceeds to buy back shares and fund acquisitions. Operating cash flow in FY2025 was $1.234B, compared to $1.059B in FY2024 — a 16.5% increase (adjusted for that one-time $66M tax payment, underlying growth was over 23%).

The buyback program is massive and shareholder-friendly. In FY2025, they repurchased 6.8 million shares for about $1.4 billion. At a $171 stock price today, that means they’re aggressively buying their own stock even as it falls — which management does when they think the stock is cheap.

One flag worth noting: working capital has been declining steadily over three years. Working capital — which is simply current assets minus current liabilities — was $626M in FY2021, fell to $493M in FY2022, $342M in FY2023, and reached $249M by end of FY2024. The current ratio (current assets divided by current liabilities) has dropped to around 1.14-1.16x as of the most recent period, which is below Check Point’s own 10-year historical median of 1.56x. A current ratio above 1.0 means they can still cover short-term bills comfortably — but the trend is tightening.

Why is working capital shrinking? Because deferred revenue (subscriptions customers pay upfront but Check Point recognizes over time) keeps building on the liability side. This is actually a good kind of working capital pressure — it reflects growth in subscription bookings, not operational stress. The Remaining Performance Obligation (RPO) — a forward-looking indicator of locked-in future revenue — stands at $2.73B as of Q4 2025, up 8% year-over-year. That’s essentially guaranteed future revenue already in the bag.

SECTION IV: Fundamental Valuation Metrics & Investment Call

Let’s do the math in plain English.

P/E Ratio: At $171.48 and GAAP EPS of $9.62, you’re paying about 17.8x earnings. On Non-GAAP EPS of $11.89, it’s closer to 14.4x. For context, Check Point’s 5-year average P/E has typically ranged between 20x and 25x. At 17-18x GAAP earnings today, this is one of the cheapest it’s been in a long time. The cybersecurity sector median P/E trades closer to 40-50x for high-growth names (think CrowdStrike, Palo Alto). Check Point’s multiple is so low because the market doesn’t give it a “growth stock” premium — but it also means the downside is limited.

Free Cash Flow: Operating cash flow was $1.234B in FY2025. Capital expenditure is minimal for a software-heavy company (they paid ~$160M for land for their new Tel Aviv campus in Q3 2025, but that’s a one-off). Recurring FCF is well above $1.1B annually. At an $18.4B market cap, you’re paying roughly 16-17x free cash flow. For a company growing earnings double digits and buying back stock, that’s genuinely attractive.

Margins: Gross margin is around 87% — typical for a software/subscription business. Net margin hit 38.8% in FY2025. Operating margin was 30.5% on a GAAP basis. These are elite numbers. Very few $18B companies are this profitable as a percentage of revenue.

Dividends/Buybacks: No dividend — but Check Point does something arguably better. They buy back their own stock aggressively. $1.4 billion returned to shareholders in FY2025 alone. That’s nearly 8% of the entire current market cap returned in one year. That’s a powerful shareholder return mechanism.

Liquidity Check: The quick ratio (cash + receivables divided by current liabilities) is comfortably above 1.0. The company has zero traditional bank debt — the only debt is the new $2B convertible notes issued in December 2025. With $4.34B in liquid assets against those notes, there’s no solvency concern whatsoever. The declining working capital ratio is a nuance of subscription accounting, not a red flag.

The Call: Hold, with conviction to buy on further weakness toward $160-$165. The business is fundamentally strong. The stock is cheap. The problem is Q1 2026 revenue guidance came in well below Wall Street expectations ($655M-$685M vs. ~$746M consensus). That gap is real and reflects a transition year as new AI products scale. If you can handle 6-12 months of potential sideways movement, CHKP at these levels is a patient accumulator’s dream.

SECTION V: Long-Term Outlook & Risk Assessment

The tailwind for Check Point could not be better. Cyberattacks globally hit record levels in 2025 — nearly 2,000 weekly attacks per organization on average, according to the company’s own threat intelligence data. Every company, government, and hospital in the world needs exactly what Check Point sells. AI is making hacker attacks faster, smarter, and harder to detect — which paradoxically is great for cybersecurity vendors.

Management’s four strategic pillars — Hybrid Mesh Network, Workspace Security, Exposure Management, and AI Security — are all growing. Security subscription revenue is the key number to watch: $1.22B in FY2025, up 10%. If that growth rate accelerates to 15%+ over the next two years, the stock re-rates quickly.

The 5-year FY2026 EPS guidance is $10.05-$10.85. At a fair-value multiple of 22x earnings (still conservative for cybersecurity), that puts the stock in the $220-$240 range. If they can accelerate growth and justify 25x earnings by 2028-2030 on ~$14-15 EPS (plausible with buybacks shrinking share count), you’re looking at $350-$375. That’s a 100-120% return from today over 4-5 years — roughly a 15-20% annualized return.

Real Risks — Don’t Ignore These:

Revenue growth slowdown is the obvious one. Check Point grew 6% in FY2025. If that number doesn’t improve meaningfully in FY2026-27, the stock stays cheap and stuck. Management has guided Q1 2026 revenue 12-15% below what analysts expected — that’s a meaningful miss on guidance and is keeping a lid on the stock right now.

The new $2B in convertible notes changes the financial profile. Check Point was debt-free for years. Now it has leverage. If interest rates stay high, those notes become more expensive to service — though with $4.3B in cash, this is more optics than real danger.

Geopolitical risk is real. Check Point is an Israeli company with offices in Tel Aviv. The region remains volatile. Any escalation in Middle East tensions could disrupt operations or create regulatory complications in certain markets.

Competition is fierce. Palo Alto Networks, CrowdStrike, Fortinet, and Microsoft are all fighting for the same enterprise security budgets. Microsoft in particular is bundling security features into its enterprise subscriptions, which can squeeze vendors who sell standalone security products. Check Point’s answer is the Infinity Platform — one integrated platform to rule them all — but the battle is real.

The declining working capital ratio bears watching. While the current explanation (deferred subscription revenue) is benign, any deterioration in the underlying business would make this a more serious signal. Track it quarter by quarter.

Disclaimer: This content is for educational and informational purposes only. It does not constitute financial, investment, or legal advice. I am an AI, not a certified financial advisor. Please do your own due diligence or consult a certified professional before making any investment decisions.