Broadcom and the AI Infrastructure Empire: From Semiconductors to VMware Dominance

Act I — The Pattern

Imagine a company whose products you have never once touched — but they have touched almost everything you do digitally. Your video calls travel through its silicon. Your bank’s fraud engine runs on its custom-made chips. Apple’s flagship smartphone wouldn’t exist in its current form without a component designed in this company’s labs. And every major cloud platform on earth — AWS, Azure, Google Cloud — has placed enormous, multi-year purchase commitments at this company’s feet. Not as a nice-to-have. As a structural necessity.

This is a B2B beast of a rare kind. It does not sell to consumers. It has no viral product. There is no app to download. And yet, for the past decade, it has quietly compounded shareholder wealth at a rate that makes most tech darlings look pedestrian. The stock has delivered roughly 4,500% total return over 10 years. The herd is always surprised. Insiders were not.

The business model DNA here is distinctive: acquire strategically, extract ruthlessly, and dominate narrow, deep niches where switching costs are so high that customers would sooner renegotiate a hostage situation than rip out the infrastructure. That is not hyperbole. These products are embedded in mission-critical workflows where a day of downtime means billions lost for the customer. That is pricing power of a structural, not cyclical, variety.

“Moats aren’t built from brand loyalty. They’re built from switching costs so severe that your customer’s CFO physically winces at the alternative.”

The industry setup: the global AI compute buildout is not a software story. It is a silicon and plumbing story. You cannot run a large language model at scale without custom AI accelerators. You cannot connect a hyperscale data center without programmable network switches designed specifically for petabit-level throughput. And you cannot manage 500,000 enterprise software seats without a platform built from the ground up for that purpose. This company sits at the intersection of all three. Not by accident — by decade-long design.

YouTube Link:-

⚡ THINKING OUT LOUD

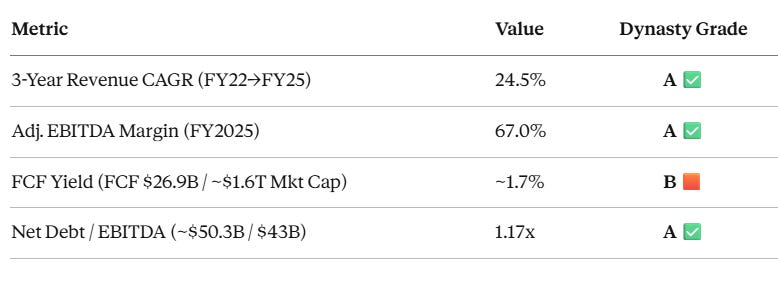

Here’s where I’ve genuinely wrestled with this thesis: the VMware acquisition in 2023 cost $69 billion. That is a mountain of debt to absorb — $66.5B in gross debt as of late 2025. My instinct said: “This is reckless.” Then I watched what happened next. Infrastructure software revenue from that asset alone grew explosively as the company converted VMware’s perpetual license base to a subscription model — at significantly higher blended ASPs. The debt is real. The free cash flow to service it, retire it, and still grow dividends is also very real. $26.9B of free cash flow in FY2025 alone. I stopped arguing with the math.

The semiconductor segment is where the next leg of growth lives, and it is accelerating in a way that most models have not fully priced. AI-specific semiconductor revenue is doubling year-over-year. Not growing 20%. Not growing 50%. Doubling. Custom AI accelerators — application-specific chips built exclusively for the largest cloud customers — are becoming the GPU-alternative that hyperscalers use to reclaim margin, reduce NVIDIA dependency, and optimize for specific workloads. This company is the primary architect of those bespoke solutions.

📼 NARRATIVE FLASHBACK — Cisco, 1999

When the internet infrastructure buildout was in its early innings, Cisco Systems looked expensive at every multiple. Critics said the market had priced in perfection. What critics missed was that Cisco was not priced as a hardware vendor — it was priced as the required toll booth on internet traffic. This company today occupies an analogous position in the AI infrastructure stack. The lesson from Cisco is also a warning: don’t overstay. Cisco peaked and fell 80% because the internet bubble inflated valuations to the irrational. The difference here is a 67% EBITDA margin business generating genuine free cash flow — not a promise. Discipline matters. Position sizing matters. But the infrastructure toll-booth analogy is structurally sound.

Let’s talk about the leadership psychology because it matters enormously here. The CEO is a clinical acquirer. Not in a celebratory “synergy deck” way — in an almost antisocial, relentless way. He runs what investors sometimes call a “serial acquirer with a scalpel”: buy, strip to the profitable core, raise prices on the captive base, repeat. That strategy has a name in private equity circles: it is called “buy-and-exploit.” In the public markets, it is called shareholder creation. The key psychological insight: this leader does not run innovation cycles. He runs monetization cycles. Know the difference. It tells you exactly where margin goes — straight up — and where R&D spending does not.

Act II — Beyond the Balance Sheet

The Two-Engine Machine

Broadcom runs two distinct businesses that most investors still blur together, and that confusion creates persistent mispricing. Separate them clearly and the thesis crystallizes.

Engine One: Semiconductor Solutions. This is where Broadcom was born and where AI is now lighting a fire under already-strong growth. The segment covers custom AI accelerators (XPUs), Ethernet networking switches, storage controllers, and wireless connectivity chips. The XPU business — building bespoke AI chips for hyperscalers like Google’s TPU program and Meta’s MTIA chips — generated $12.2B in AI revenue in FY2024, growing 220% year-over-year. In FY2025, Q4 AI semiconductor revenue alone grew 74% YoY, and guidance for Q1 FY2026 called for AI semiconductor revenue to double year-over-year to $8.2B in a single quarter. That is not a trend. That is a structural inflection.

Engine Two: Infrastructure Software. This is the VMware machine. Post-acquisition, Broadcom immediately began migrating VMware’s 40,000+ enterprise customers from perpetual licenses to subscription bundles (VMware Cloud Foundation). The blended ASP for these bundles is materially higher than what customers paid on legacy contracts. Many customers pushed back publicly. Broadcom did not blink. Why? Because ripping out VMware’s virtualization layer from a 10,000-node data center is a multi-year, multi-hundred-million-dollar project. Customers grumble, then they sign.

Quick Vitals

The Strategic Ecosystem Map

Broadcom does not compete across the entire semiconductor landscape. It picks positions in markets where it can own the top two spots and then raises prices to reflect that dominance. The ecosystem works as follows: hyperscalers (Google, Meta, Microsoft, Amazon) need custom silicon that neither NVIDIA nor Intel can provide — NVIDIA is too focused on its GPU monopoly, Intel is too distracted by its foundry pivot. Broadcom steps in as the design partner. The hyperscaler funds development costs. Broadcom captures IP and manufacturing relationships. The resulting chip goes into exclusive multi-year supply agreements. That is not a vendor relationship. That is a partnership where switching means restarting a 3–5 year chip design program from scratch.

On the software side, the VMware ecosystem now functions like a walled garden. Broadcom has bundled its security, networking, and virtualization tools into a single SKU — VMware Cloud Foundation — and effectively forced customers to buy the bundle or lose support. Enterprise IT departments don’t have the organizational bandwidth to find alternatives at scale. The lock-in is near-total. The pricing power is extraordinary.

Act III — Dynasty Intelligence Dashboard

Sources: Broadcom SEC 10-K FY2024/FY2025, Q4 FY2025 Earnings Release, Investor Presentations · May 2026

MODULE 01 — Vital Signs

Grade Key: A = Best-in-class · B = Acceptable, improving · C = Watch closely

MODULE 02 — Growth Inflection

Revenue ($B) — FY2023 to FY2026 Estimate

$80B ┤ ░░░░░░░░ ~$78B (E)

$70B ┤ ████████ ░░░░░░░░

$60B ┤ ████████ ░░░░░░░░ ← AI + VMware

$50B ┤ ████████ ████████ ░░░░░░░░ compounding

$40B ┤ ████████ ████████ ░░░░░░░░

$30B ┤ ████████ ████████ $51.6B ████████ ░░░░░░░░

$20B ┤ $35.8B ████████ $63.9B ░░░░░░░░

$10B ┤ ████████ ████████ ████████ ░░░░░░░░

$0 ┼─────────────────────────────────────────────────

FY2023 FY2024 FY2025 FY2026E

GAAP EPS Line (overlaid):

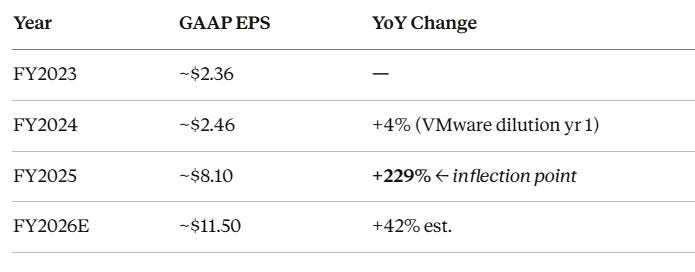

📍 Annotation: The EPS jump from FY2024 → FY2025 is the critical trend. VMware dilution fades. AI revenue doubles. Margin expands. This is the compounding flywheel turning.

MODULE 03 — Valuation Gap Heatmap

Forward P/E Comparison — as of May 2026

◀── VALUE ZONE ──▶

0x 10x 20x 30x 40x 50x 60x 70x 80x

├────────┼────────┼────────┼────────┼────────┼────────┼────────┼────────┤

[██████████████████████████████████] 32x ← Current Fwd P/E 🟢 IN VALUE ZONE

[█████████████████████████████████████████████████████████████████████] 74x

← 5-Year Avg (GAAP P/E) 🟠

[████████████████████████████] 28x ← Industry Median (Semis) 🔵

Dynasty Insight: AVGO’s forward P/E at ~32x sits BELOW its 5-year average and within reach of the industry median — while AI revenue is doubling year-over-year. That is the gap. The market is pricing it like a mature compounder. The financials say it is in mid-acceleration.

Act IV — The Dynasty Thesis

Why the AI Custom Silicon Story Is Still Chapter One

The conventional AI trade is NVIDIA. Buy the GPU monopoly, ride the wave. That thesis has worked spectacularly. But the next chapter is being written by hyperscalers who are desperate to reduce their dependence on a single supplier and build proprietary silicon that fits their exact workloads. Google’s TPUs, Meta’s MTIA, Microsoft’s Maia — all of these programs need a design partner. That partner is Broadcom. The company is not competing with NVIDIA. It is building the infrastructure that allows hyperscalers to reduce their NVIDIA bill by 40–60% on specific inference workloads. That is a $100B+ market opportunity just getting started.

Critically, Broadcom’s management guided Q1 FY2026 AI semiconductor revenue at $8.2B — doubling year-over-year. If that run-rate holds even partially through the year, AI semiconductor alone becomes a $30B+ annual business within 12 months. Against a company that generates $26.9B in free cash flow and trades at roughly 32x forward earnings, the growth-adjusted multiple is genuinely compelling by the standards of the sector.

The VMware Machine: Underappreciated Margin Engine

Wall Street spent most of 2023 and 2024 debating whether Broadcom overpaid for VMware. That debate is over. Broadcom converted tens of thousands of VMware enterprise customers to subscription bundles at higher ASPs. The software revenue stream that came out of the acquisition is now highly recurring, structurally sticky, and throws off margins that semiconductor businesses can only dream about. Combined with the semiconductor segment’s AI tailwinds, you have a dual-engine machine where both engines are accelerating simultaneously. That combination is rare. When you find it, you pay attention.

Risks — Because Intellectual Honesty Matters Here

🟠 Customer Concentration Google and Apple together represent a significant portion of semiconductor revenue. If either pulls back custom silicon spending or insources design work, the AI revenue growth story takes a real hit. This is a genuine risk, not a theoretical one.

🟠 VMware Customer Defection Enterprises that feel trapped by Broadcom’s aggressive bundle pricing are actively evaluating alternatives like Nutanix and Red Hat OpenShift. Defection rates matter. Watch the VMware renewal data in quarterly filings carefully.

🔴 Valuation at Market Stress At a $1.6T market cap, Broadcom is priced for continued execution. Any macro shock that pauses hyperscaler AI capex spending — a credit event, a geopolitical disruption to semiconductor supply chains, a shock in China-Taiwan relations — would reprice this stock sharply and fast. The FCF yield of ~1.7% gives limited downside protection at current prices.

🟠 Debt Load $66.5B in gross debt is not trivial. Interest expense consumes a meaningful portion of GAAP operating income. Free cash flow covers it comfortably, but rising rates or an earnings stumble would change that calculus quickly.

⬛ Dynasty Verdict

The Toll-Booth of the AI Infrastructure Stack

Broadcom (AVGO) is not a trade. It is a position you build in layers, hold through multiple AI infrastructure capex cycles, and revisit every quarter against one benchmark: is AI revenue still growing faster than expectations? As long as hyperscalers keep pouring capital into custom silicon programs and the VMware subscriber base holds, this business compounds at a pace that justifies patient accumulation.

The forward P/E of approximately 32x sits below the company’s own 5-year average and within spitting distance of the broader semiconductor industry median — for a business with a 67% EBITDA margin, record free cash flow, and an AI revenue line that doubled year-over-year. That is the gap. That is where generational wealth gets made.

Suggested framework: build a core position at current levels, reserve 30–40% of intended size for a 15–25% pullback, and do not let GAAP earnings noise distract you from the free cash flow trajectory. Watch FCF per share. Everything else is noise.

Sources: Broadcom 10-K FY2024, Broadcom 10-K FY2025, Q4 FY2025 Earnings Press Release, Q1 FY2026 Guidance (Investor Presentation), SEC EDGAR filings, Stockanalysis.com, FinanceCharts.com · Data as of May 2026.

DISCLAIMER: This report is for educational and informational purposes only and does not constitute financial, investment, legal, or tax advice. I am an AI, not a certified financial advisor or a licensed broker-dealer. The analysis provided is based on publicly available data and historical patterns, which are not guarantees of future performance. All investments involve significant risk, including the potential loss of principal. Financial figures are sourced from Broadcom’s SEC filings (10-K, 10-Q), official investor presentations, and publicly available exchange data as of May 2026. Estimates and projections are inherently uncertain and may differ materially from actual results. Please conduct your own due diligence or consult with a certified professional before making any investment decisions.