ADYEN N.V. (AMS: ADYEN)

SECTION I: Investment Thesis & Summary

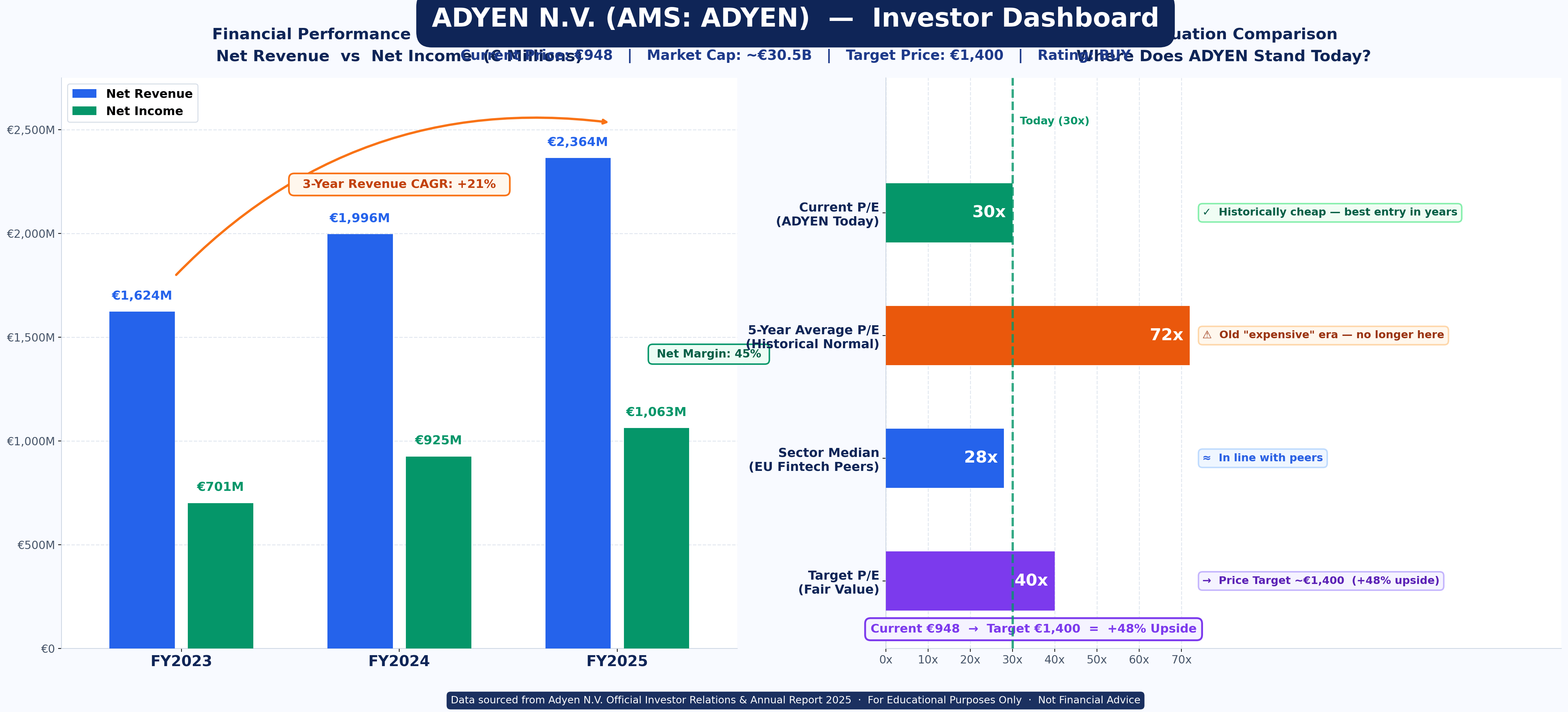

Adyen just dropped nearly 47% from its 52-week high of €1,767. The market got spooked because reported revenue growth slowed to 18% for FY2025 versus the 23% pace it ran in FY2024. But here’s what Wall Street is missing: almost all of that slowdown came from the US dollar getting weaker against the Euro. Strip out the currency noise, and Adyen is still growing at 21% in constant currency terms. The business is not broken. The stock is just on sale.

The underlying machine — a single, fully-integrated payments platform with a 55% EBITDA margin, nearly zero debt, and €1B+ in free cash flow — is stronger than ever. You’re now buying that machine at a P/E of about 30x, compared to the historical average of 70x+. That’s a rare entry point.

YouTube Demo Link:-

SECTION II: Business Model & Operations

Adyen is an Amsterdam-based fintech that does one thing with exceptional focus: it processes payments for large global businesses. Think of it as the invisible technology layer behind the “Pay Now” button at companies like Meta, Uber, Microsoft, H&M, and eBay. When you tap your card at an Uber in Tokyo or buy something from an H&M store in São Paulo, Adyen is very likely running the transaction underneath.

What makes Adyen different from Visa or Mastercard is that Adyen does everything in-house, in a single platform. It’s not just moving money — it handles the full payment stack: authorisation, risk management, processing, acquiring, settlement, and even financial products like capital lending and issuing cards to merchants’ own customers. Competitors have to stitch together five different vendors to replicate what Adyen does in one.

Geographically, about 58% of revenue comes from Europe, Middle East, and Africa. North America contributes 27%, which is the fastest-growth prize. Asia-Pacific adds 10%, with Japan and India now showing serious traction. The remaining 5% comes from Latin America.

The big recent move is Adyen’s push into Embedded Financial Products (EFP) — essentially letting Adyen’s platform customers offer banking and card services to their own end-users through Adyen. Think of a marketplace that can now offer instant payouts and a prepaid debit card to its sellers, powered by Adyen behind the scenes. Issuing volumes in this segment rose 8x year-over-year in H2 2025. Also notable: Adyen signed Starbucks and rolled out across 943 European stores in just seven weeks, which is a genuinely impressive operational feat.

SECTION III: Historical Financial Review

Let’s talk numbers. The story is simple — Adyen has been a consistent growth machine.

Net Revenue went from €1,624M in FY2023, to €1,996M in FY2024, and then to €2,364M in FY2025. That’s a 3-year revenue CAGR of roughly 21% — impressive for any company, extraordinary for one of this size. Crucially, the quality of that revenue is superb. Every euro of net revenue Adyen earns is real, cleaned-up payment fee income — there’s no hardware, no physical goods, no complicated supply chain.

Net income followed a strong upward trajectory: €701M in FY2023, €925M in FY2024, and approximately €1,063M in FY2025 — a 32% jump year-over-year in FY2024 alone. Net margin for FY2025 is running at about 45%. That’s a business that keeps nearly half of every euro it earns as profit.

EBITDA hit €1,246M for the full year 2025 at a 53% margin, up from 50% in FY2024. Management is guiding for further margin expansion toward 55%+ by 2028, while still investing in headcount (adding 550-650 people in 2026, primarily in the US and global tech hubs).

On the balance sheet, Adyen carries effectively zero financial debt — only lease obligations of around €228M. There are no bonds, no bank loans, no leverage story to worry about. That’s a management team that runs the company on its own earnings. No share buybacks or dividends have been announced, and frankly, with management focused on long-term growth, that’s the right call.

Now, working capital is where things get interesting and a bit unusual — which is why it needs explaining carefully.

SECTION IV: Fundamental Valuation Metrics & Investment Call — Working Capital & Liquidity Spotlight

Let me address the “Working Capital and Liquidity” picture head-on, because this is where most investors trip up when analysing Adyen.

The Settlement Float Effect — Don’t Panic at the Balance Sheet

Adyen holds a banking licence. That means when it processes payments on behalf of merchants, it temporarily holds huge sums of money — called settlement assets — that belong to merchants, not to Adyen. These funds appear on Adyen’s balance sheet as both an asset and a matching liability. As of FY2024, total assets were €11.4B against total liabilities of €7.2B. But the vast majority of both sides of that ledger are pass-through merchant funds — receivables on one side, payables to merchants on the other. This is not leverage. It’s settlement float, and it nets to zero.

Strip that out and Adyen’s own financial position is pristine. Here’s what actually matters:

Free Cash Flow (FCF): In FY2025, Adyen generated approximately €1.03B in free cash flow, at an 86% FCF conversion ratio. That means for every €1 of EBITDA, Adyen converted €0.86 into real cash in the bank. A conversion ratio above 80% is considered excellent in fintech; Adyen has been consistently at or above that level for three straight years.

CapEx Discipline: Capital expenditure was maintained at 5% of net revenue in FY2025 — roughly €118M. Adyen builds and owns its entire technology stack in-house, so it will always spend on infrastructure. But the CapEx commitment is predictable and well-managed. This is a capital-light business in every meaningful sense.

Debt-to-Equity: Essentially zero financial debt. Total debt-to-equity (excluding lease obligations) sits at roughly 5%, almost entirely lease liabilities for office space. This is one of the strongest balance sheets in European fintech.

Liquidity Position: Adyen holds substantial cash and liquid assets. The company’s own funds (separate from merchant settlement balances) are comfortably positive and growing. With no debt maturities to manage and €1B+ flowing in every year, Adyen is not going to run a liquidity problem anytime soon.

Valuation — You’re Getting a Bargain Here

The P/E ratio right now is approximately 30x on a trailing twelve-month basis. The 5-year average P/E for this stock has been in the 70-80x range. The sector median for high-growth European fintech sits around 28-32x. At 30x, Adyen is being priced like a slow-grower — even though it’s expanding at 20%+ per year with 53% EBITDA margins. That mismatch is where the opportunity sits.

At a target P/E of 40x applied to estimated FY2026 EPS of around €38-40, a price of €1,400 is both achievable and well-justified. That’s a 48% upside from current levels.

FCF Yield at today’s price is approximately 3.3% on a €30.5B market cap vs €1B+ FCF. That doesn’t scream “screaming bargain” but for a company compounding FCF at 25%+ annually, it is very reasonable.

SECTION V: Long-Term Outlook & Risk Assessment

The 5-15 Year Case

Management is targeting one of the largest fintech platforms in the world. That’s not just corporate cheerleading — the numbers suggest they have a credible path to get there. Processing volume hit €1.4 trillion in FY2025. The global payment processing market continues expanding as more transactions shift from cash to digital. Adyen’s platform intelligence compounds as volume grows — more transactions mean better fraud detection, better conversion rates, and more data to sell value-added services to merchants.

If Adyen maintains 18-20% annual net revenue growth for the next five years and expands EBITDA margins toward 58-60%, EPS could comfortably reach €80-100 by FY2031. At a conservative 35x P/E, that implies a price of €2,800-3,500 over that horizon. That’s a potential 3-4x from today’s price — or roughly 200-280% total return over five to seven years.

Real Risks — Don’t Ignore These

Currency headwinds are real and lasting. A significant chunk of Adyen’s processed volume comes from customers that bill in US dollars, so a weak USD directly cuts into reported euro revenue. This is what caused the 2025 “slowdown” that spooked the market, and it may persist into H1 2026 as management noted.

Competition is intensifying. Stripe, Worldpay, and PayPal are all fighting for the same enterprise payments clients. While Adyen’s integrated platform gives it a strong moat, winning new large enterprise accounts is a long, expensive sales cycle — and losing one (as it lost a large-volume customer in 2025 which distorted processed volumes) can move the needle on reported numbers.

ECB rate cuts change the interest income picture. Adyen earns meaningful interest on the merchant balances it holds at central banks and commercial banks. As the ECB cuts rates, that interest income will compress. It’s not existential, but it’s a headwind worth tracking.

Regulatory risk is always in the background for any firm with a banking licence operating across 40+ markets. A significant regulatory change in the EU payments landscape, changes to interchange fee rules, or unfavourable ECB capital requirements could affect the business model.

Valuation re-rating risk: if growth slows further or misses expectations, the stock could re-price to 20-25x, implying further downside to €700-800 before recovering.

Simply put: Adyen is a high-quality business temporarily out of favour. The liquidity position is fortress-strong, the FCF is real, the debt is non-existent, and you’re paying a historically low multiple for it. The risk is that you might wait 12-18 months before the market agrees with you.

Disclaimer: This content is for educational and informational purposes only. It does not constitute financial, investment, or legal advice. I am an AI, not a certified financial advisor. Please do your own due diligence or consult a certified professional before making any investment decisions.